Black Swan Outlook

December: The three worlds of 2025

On Sunday, we published our optimistic and pessimistic scenarios for 2025. In this Outlook we outline the scenario we consider the most likely one (the consensus scenario). We also provide forecasts for growth of gross domestic product (GDP) for the three scenarios, forecasts for stimulus of China, and the likelihoods of the three scenarios.

Our most likely scenario for 2024 was fairly accurate. Only the stagnation of the U.S. economy and the recession of the Eurozone did not come to be. However, the private sector of the U.S. looks to be in a recession and many countries of the Eurozone are in de facto recession (e.g., Germany and Finland).

Our most likely scenario indicates that 2025 would be the year, when the first clear signs of the multifaceted economic crisis, the ‘perfect storm’, would appear. We have been warning on it since 2017. These signs can include renewed banking sector issues (runs and failures), capital market issues (failed auctions, soaring yields) and a wide variety of negative developments in the real economy (e.g., a notable increase in bankruptcies). Yet, we do not expect an outright economic collapse to appear next year, while it’s definitely within the realms of possibilities.

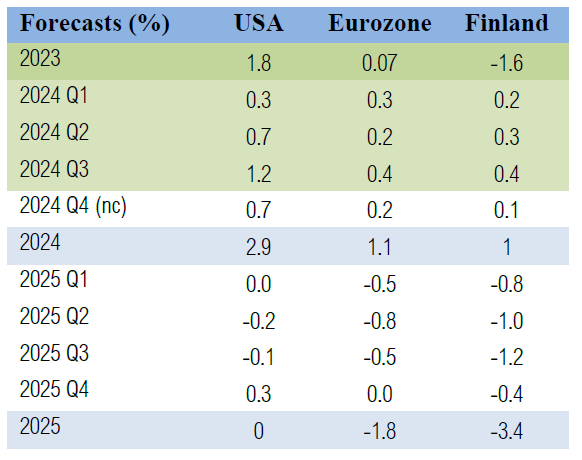

GDP Forecasts

Our nowcasts (nc) are essentially unchanged from past month.1 We forecast that the U.S. economy would have grown at a rapid 0.7% (2.8% annualized) rate during this quarter, while the Eurozone and Finnish economies would have seen a more modest growth. Please note that nowcasts are the same for every scenario.

The Optimistic Scenario

We start with the GDP forecasts of our optimistic scenario detailed in the Weekly Forecasts Year-End Special.

Notably, the U.S. economy would grow through the 2025, but with a lacklustre rate. The Eurozone and Finnish economies would experience a mild-to-moderate contraction in 2025. This is due to the combination of policies of President Trump aimed at scaling back the gargantuan fiscal stimulus enacted by President Biden, and re-capitalization of European and U.S. banks which halt the looming financial collapse. There’s global recession, but it’s a shallow one.

We have to emphasize that the GDP growth can be notably higher, if central banks start to add artificial liquidity into the markets through QE-programs, again, and if governments keep on running fiscal stimulus at full blast. This would lead to greater economic momentum, but at the cost of growing the global imbalances (debt, zombification and asset bubbles) further, while ensuring even bigger collapse in the future (see the Weekly Forecasts). Lacking this, we forecast the economic momentum of the world economy to slow in 2025 also in the optimistic scenario.

The Pessimistic Scenario

In the pessimistic scenario, we assume that the deepening escalation in Ukraine and in the Middle East push in motion the third wave of the global financial crisis during H1. A war in the Middle East leads to another and a more severe energy shock causing inflation to shoot up forcing central banks to enact another round of rate rises. These, combined with serious capital market issues, push the world economy in a downward spiral which deepens throughout the year. The abysmal GDP forecasts reflect this.

The Consensus Scenario

Our most likely scenario is actually rather close to the optimistic scenario, GDP-wise. This is because we continue to assume that fiscal stimulus will be kept running, even though in diminished volumes in the U.S. and China, in 2025. This will carry the world economy for one more year. See a more detailed explanation of the scenario below.

So, according to the forecast we consider most likely, there would be no economic collapse next year. However, some serious reservations need to attached to this forecast.

In this scenario, we are essentially assuming that ALL key players in the global economy, i.e., governments and central banks of China, the Eurozone and the U.S. act in cautious manner. All actions are assumed to be gradual and measured (see below). This may not come to be. This is why our scenario likelihoods are heavily tilted on the pessimistic side (see the Conclusions), implying that the developments we are likely to see are going to be some combination of the Pessimistic and Consensus scenarios.

Forecasts on the stimulus of China

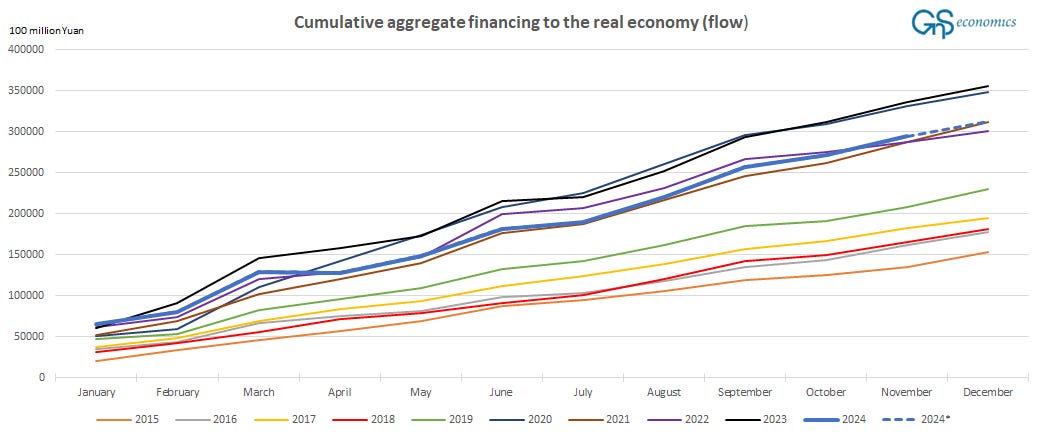

Steady on. The flow of aggregate financing grew by RBM2.326 trillion in November, which was mostly in-inline with past year’s RMB2.455 trillion. Our forecast indicated that the November flow would have been RMB2.487 trillion, and so it was rather accurate. Updated forecasts indicate the flow of financing into the Chinese economy to total RMB31.2 trillion in 2024, a decline of RMB4.366 trillion from the forecast of previous month. This implies that 2025 will start with wavering global economic momentum.

The flow of financing to the Chinese economy now looks to end the year at par with that of 2021, i.e., clearly below the two “great stimulation” years of 2020 and 2023. This can be seen as a balancing act between the needs of the economy (de-leveraging) and the needs of the China Communist Party (CCP) to keep people satisfied to their rule. In October 2017, after we had discovered the massive role of China plays in the world economy, we noted:

What will China do? China prefers stability, but are they willing to allow for short-term instability to sustain long-term goals? No one knows. Nevertheless, one thing is certain: China cannot grow out of its mountain of debt. Thus, a hard landing seems unavoidable, and the world should be prepared for it.

We look to be at the cusp of another effort to balance between these short- and long-term goals of the economy vs. the CCP.

As an interesting development, foreign-currency denominated loans have now declined for 10 consecutive months, while asset-backed securities of depository institutions have declined for the whole year. These are signs that foreign funding is drying up and that banks are trying to de-lever their positions linked to the collapsed housing sector. These indicate that de-leveraging of the Chinese economy has been running in the background throughout the year.

Economic Indicators

United States, December (November)

Richmond Fed manufacturing: -10 (-14)

Empire State manufacturing: 0.2 (31.2)

Dallas Fed manufacturing: 3.9 (-0.9)

Kansas Fed manufacturing: -4 (-2)

Manufacturing PMI:2 48.3 (49.7)

Services PMI: 58.5 (56.1)

Consumer Confidence:3 104.7 (112.8)

U.S. leading indicator, November (October):4 99.7 (99.5)

Eurozone, December (November)

Manufacturing PMI: 45.2 (45.2)

Services PMI: 51.4 (49.5)

Germany ifo Business Climate:5 84.6 (85.6) (the index has been trending down since June)

China, November (October)

Caixin manufacturing PMI: 51.5 (50.3)

NBS manufacturing PMI: 50.3 (50.1)

Caixin services PMI: 51.5 (52.0)

The Consensus Scenario for 2025

To be honest, constructing the most likely path for the world economy for 2025 is exceptionally challenging. This is because there are multiple possible paths ahead depending almost solely on the decisions of the authorities and political leaders. Our most likely scenario is based on two assumptions:

Keep reading with a 7-day free trial

Subscribe to GnS Economics Newsletter to keep reading this post and get 7 days of free access to the full post archives.