Contents:

The economic outlook of China.

The Grand (Unified) Geopolitical Theory, Part I: Ensuring U.S. dominance through a conflict in Europe.

Forecasts for aggregate financing of the economy of China.

I could say that we are finally here. It’s my habit to write an introduction after the analysis is done; a practice that originates from my academic career, during which I authored or co-authored 10 peer-reviewed and several non-peer-reviewed articles. What I mean by “finally here” is that I feel that Weekly Forecasts has finally found its intended structure after “wandering in the shadows” for a year and a half.

In these third weekly forecasts of the year, we detail the economy outlook of China and provide an update to our forecasts on the financial flows to the Chinese economy for 2026. However, the main part of these forecasts is an introduction into my geopolitical-theory framework, which goes under the working title the “Grand (Unified) Geopolitical Theory.” In it, I aim to combine everything I have learned about geopolitics since my early introduction to it, when I was just 13 years old.

In this first part of the theory, I will outline the founding principle of the theory and formulate a theory explaining the war in Ukraine. One of its building blocks is the aimed destruction of the ‘Eurasian alliance,’ which I first learned about in May 2022 from a long-time U.S.-based political journalist, whose name and actual text I have been unable to locate.

The theory and its application paint an unstable near-future for Europe. It also explains why the war in Ukraine has come to be and why peace is so difficult to achieve there. Everything starts with the collapse of the Soviet Union and the resulting failure of the global superpower-stucture. As this is a theory under construction, all comments are highly welcomed.

Tuomas

The economic outlook: China

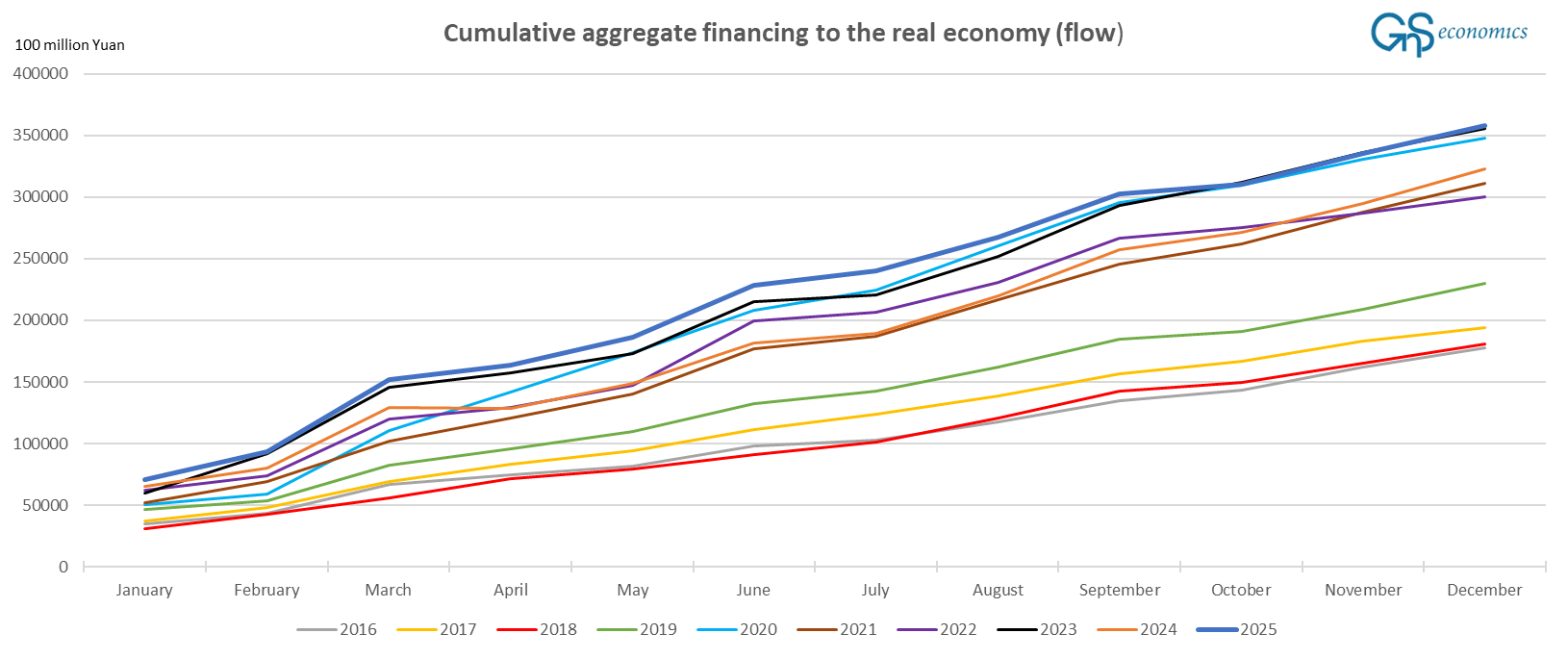

We have a record!

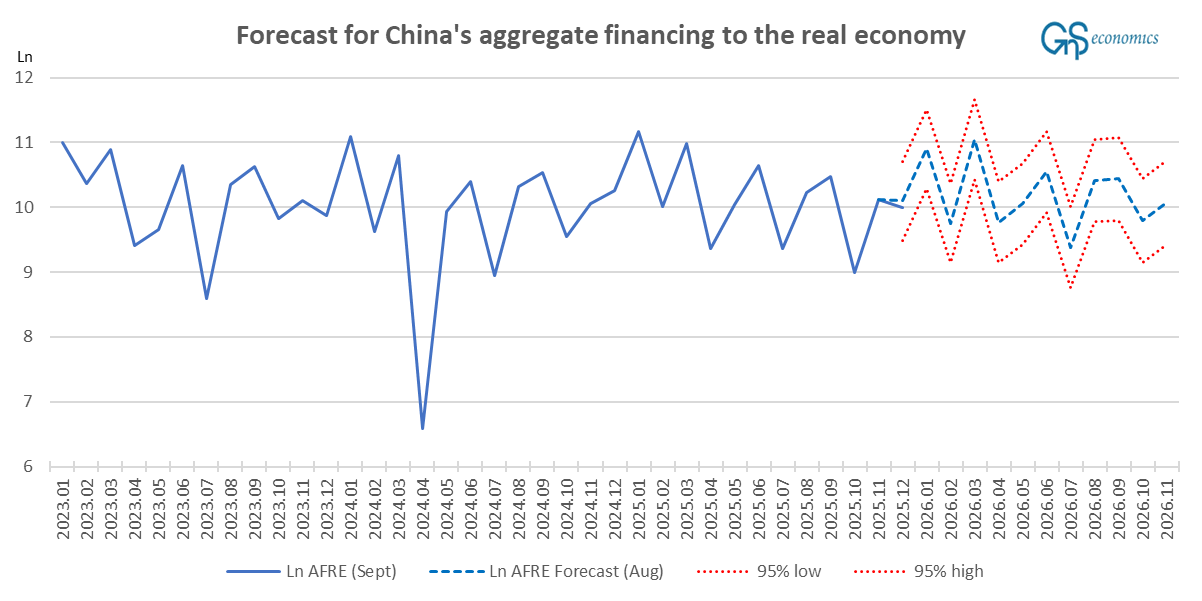

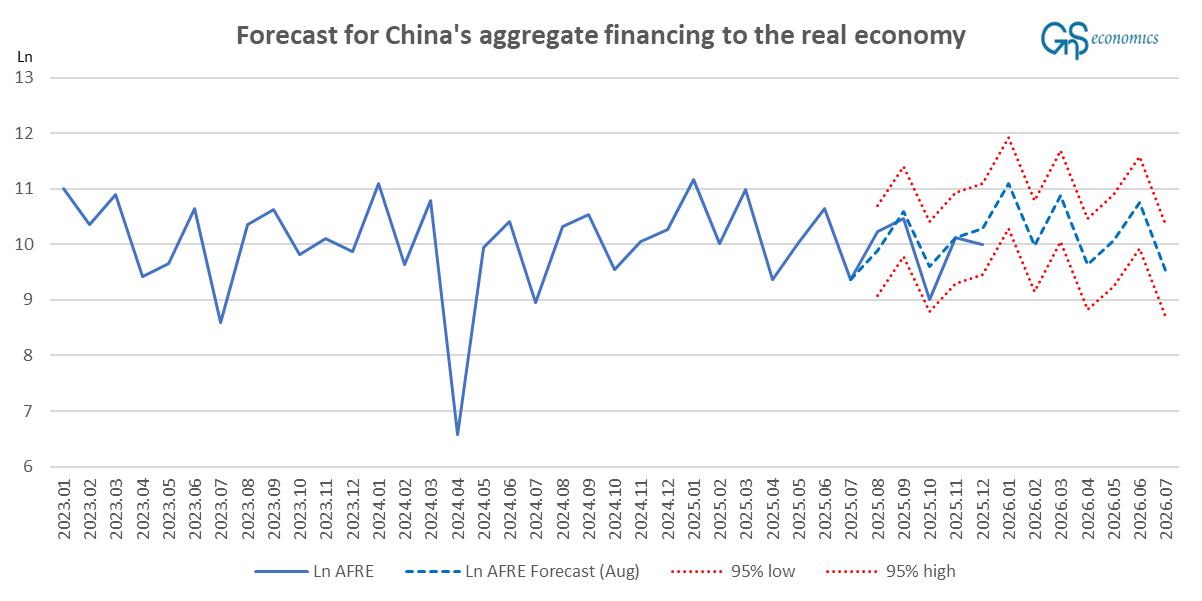

The accumulated flow of financing to the Chinese economy reached CNY 35.784 trillion in 2025, surpassing the previous record of CNY 35.569 set in 2023. In December, the flow of credit entering the Chinese economy grew by CNY 2,210 billion, which was clearly below the December record of CNY 2,851 billion set in 2024. Still, the December flow of financing was the third highest since our records began (2012). Our forecast for the flow of financing from the past month (in natural logarithms) was accurate, as shown by the figure below.

The realized figure of China’s ‘Social financing’ in December was also safely within the 95% confidence intervals of our August forecast.

Essentially the December figure indicates that the Chinese economy is likely to continue to “muddle through” the H1, like we anticipated a month ago.

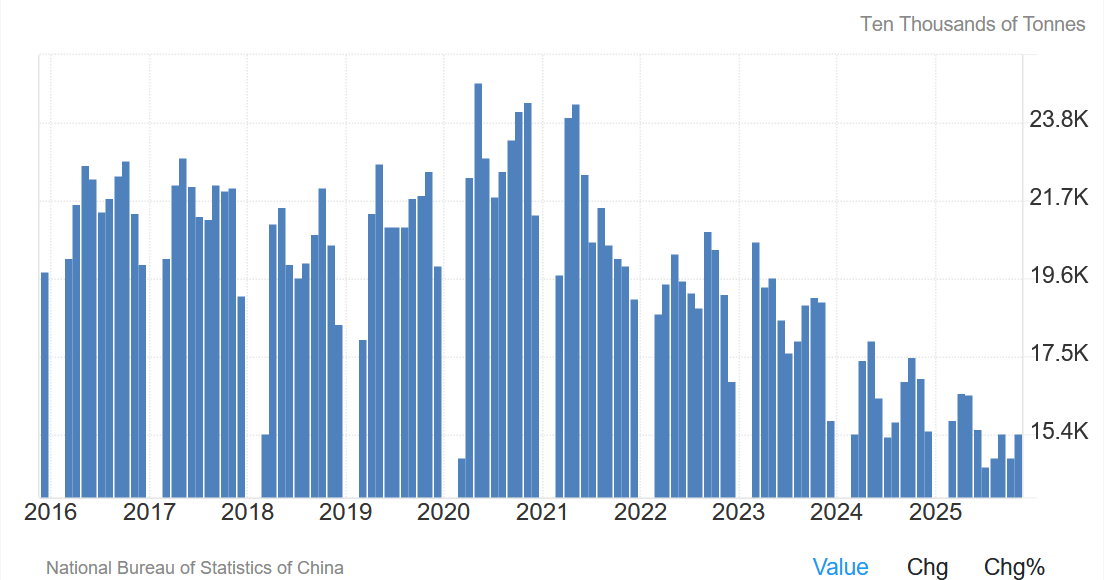

Another measure we have been using to assess the outlook of the Chinese economy has been cement production. We have used this measure because around the mid-2010s, the gross domestic product series of China became heavily manipulated. One researcher at the Bank of Finland Institute for Emerging Economies, BOFIT, noted in a lecture at the University of Helsinki that Tuomas attended that the series of China’s GDP should not be used in forecasting, because the final figure is always decided by the Prime Minister. There is also statistical evidence of the GDP series of China being “manufactured,” but we do not go there now. However, there’s no point in trying to manipulate the cement production series, which is why we have trusted it the most. Figure 4 presents the monthly series of cement production in China for the past 10 years (note that January and February data is periodically missing).

What you notice is a steady decline in the cement production starting in around mid-January 2021. However, like we noted in Weekly Forecasts 10/2025, the forecasting ability of the cement production has declined because Beijing has directed funding away from the real estate sector, which has reached a state of collapse as a result.

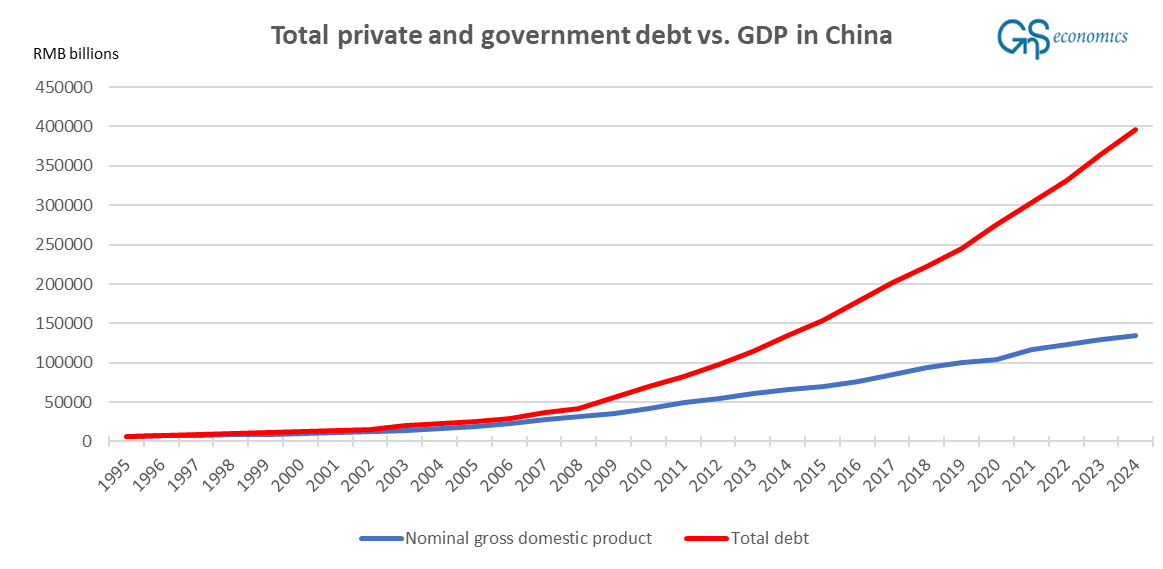

This process of blowing one debt bubble after another is the way Beijing has been able to avoid the collapse of the Chinese economy under the massive and ever-growing debt bubble. Beijing holds something of a command-and-control grip on the Chinese banking sector, which means that it can order banks to lend and direct their lending to different sectors. During the past five years, following the enactment of the “three red lines” policy concerning the real estate sector in August 2020, we have seen this in full-swing with Beijing directing the debt creation to manufacturing and AI sectors. The problem Beijing has is that to keep economy growing, debt needs to grow much faster. This has led to the economic “perversion” shown in Figure 5.

Even in a command-and-control economy this cannot be sustained indefinitely. At the end of 2024, the debt-to-GDP ratio of China stood at staggering 294%, and we do not consider this to hold all the debt.

The question for China’s outlook is, will Beijing be able to contain the collapse to the real estate sector? While it currently looks so, we have our doubts. We return to this later.

The failure of the superpower-structure and the control of Europe

Many have viewed the recent developments in the geopolitical (global) arena with worry. This, naturally, includes us. We have been analyzing, speculating on, and forecasting dire developments during the past two years, of which a worryingly high percentage has become a reality. What we will present, or start to sketch here, is a Grand (Unified) Geopolitical Theory mapping the geopolitical transition, or a rupture, as (blatantly) put by Canadian Prime Minister Mark Carney in Davos earlier this week This effort aims to connect seemingly unrelated yet coordinated geopolitical developments that have unfolded globally over the past 30 years, launched by the fall of the Soviet Union. The theory will have a central role in this section in the coming months.

The collapse of the Soviet Union led to the failing of the superpower-structure, which had dominated the world since the Second World War. Many still consider that the creation of the supranational-structure, enshrined in the supranational entities, like the United Nations and the International Monetary Fund, was behind the long period without major wars in Europe and relative calm elsewhere. However, recent developments reveal that it was actually the superpower-structure that enforced the period of (relative) peace and prosperity in Europe and the ability of the supranational structure to function (somewhat) properly in the world. The failure of the one superpower, the Soviet Union, caused the ambitions of the other superpower (the U.S.) to be unleashed, leading us to the current predicament.

What makes this so detrimental for the world is the fact that the strongest “glue” holding an empire and a nation-state (or a state-nation) together is a threat. A threat of a foreign enemy attacking the values of the nation entity or destroying it. This leads to the first founding principle of the Grand (Unified) Geopolitical Theory,1 which is that the survival of an empire, a nation holding a global hegemony, requires an enemy, true or imagined. An “enemy” feeds the drive for policies undermining the needs of the people on behalf of investments in defense industries. It creates the justification for silencing dissidents and enacting control measures to “protect” the populace. Most importantly, however, a threat of an enemy creates a justification for strong leadership, which is oftentimes epitomized in the form of a strong leader.

Europe became the epicenter of the failure of the superpower-structure essentially right after the fall of the Soviet Union. The enlargement of both the North Atlantic Treaty Organization, or NATO, and the creation of the European Union in 1993 are symptoms of this. In February 2022, the failure of the superpower-structure led to the first major war on the European continent since 1945.