Contents:

The bailout of the U.S. private credit sector continues unabated.

The two statistical dimensions of U.S. repo markets.

Is a third bailout channel of Private Credit operating through U.S. repo?

There is a serious problem brewing in the private credit sector. I have been detailing the (major) issues there since late October.

Just two weeks ago, I explained why U.S. commercial banks were so deeply “on the hook” with the issues emerging in the sector. Three weeks ago, we detailed the “hidden bailout” of the private credit sector by large commercial banks of the U.S.

This week we expose more problems in the U.S. financial system while uncovering another likely bailout channel of Private Credit running through repo. We use time series analysis to uncover the statistical drivers of repo rates. They reveal that there are indeed two sets of drivers at play, like I suspected some months ago there would.

Based on these findings, we extend the financial structure of a credit fund I unveiled two weeks ago. It reveals a similar structure that was behind the financial collapse of 2008. The private credit sector is likely to be much more levered than what is generally understood or acknowledged.

Tuomas

The bailout of the U.S. private credit sector continues

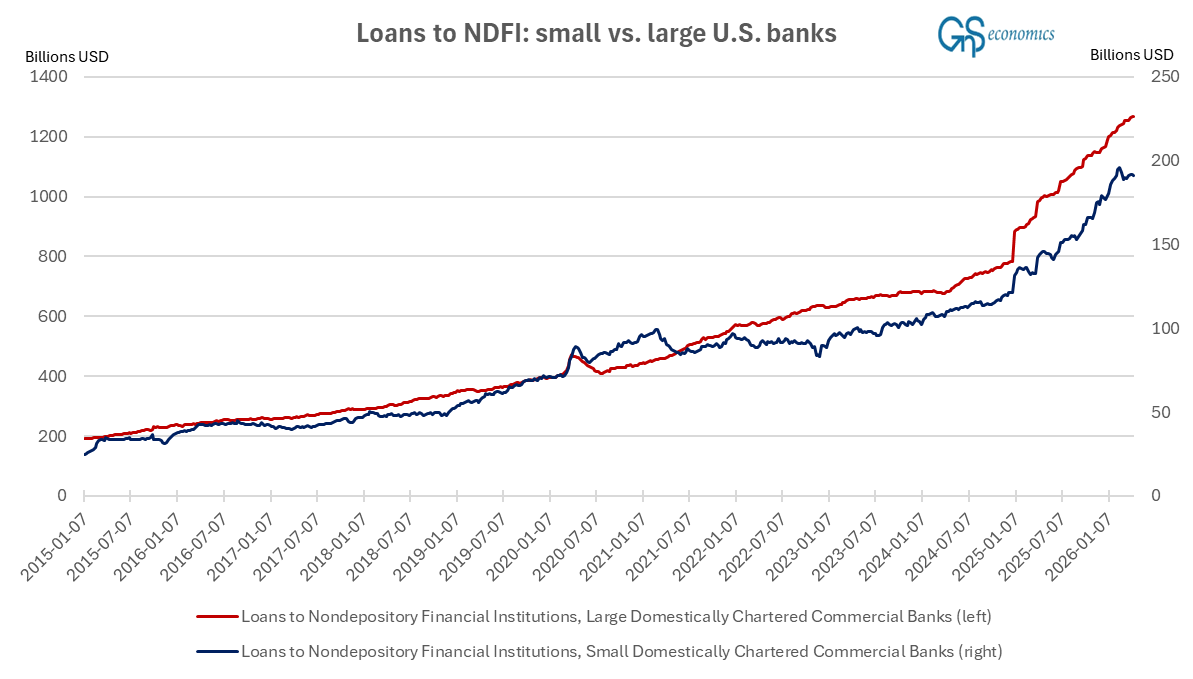

Large U.S. banks have continued to grow their lending to the non-depository financial institutions (NDFIs) in a relentless manner in April. Similarly, smaller banks have continued to shy away from the battered sector.

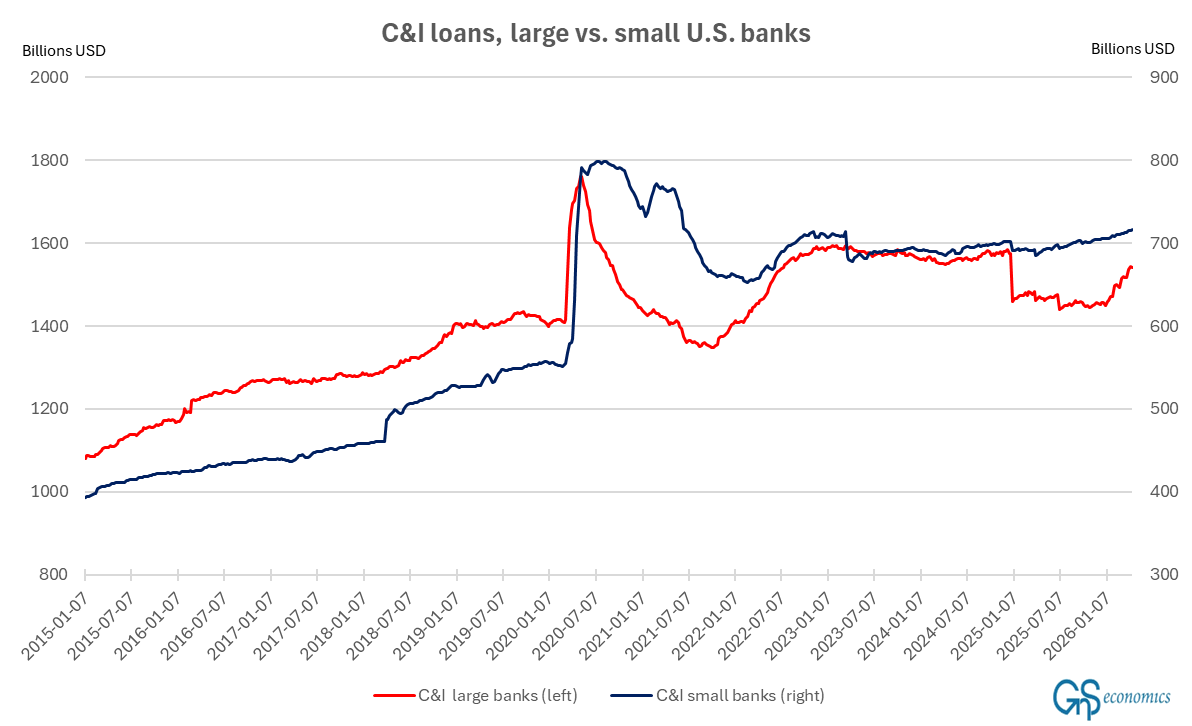

A similar pattern has continued in business lending. Figure 2 depicts the commercial and industrial loans issued by large and small U.S. commercial banks.

Big banks have continued to increase their lending to SMEs (small and medium-sized enterprises), while business lending of small banks remained stagnant (stable). There’s also an interesting pattern emerging, where the business lending of large U.S. banks grows massively during the first week of the month and then cools off.

At this point, we have no knowledge of what would be the reason behind this, but the growth is notable and highly seasonal. During the first week of February, the business lending of large U.S. commercial banks grew by 1.7% and remained subdued for the remainder of the month. The same occurred in March with a growth of 1.5% during the first week, after which the weekly growth rates fell close to zero or even to negative. The first week of April saw a growth of 1.3%. For some reason, U.S. banks thus look to push loans to businesses at the beginning of the month. Whether this relates to the bailout of the private credit sector, e.g., in some accounting-sense, remains unknown at this point.

It thus now looks that both large U.S. commercial banks and the Federal Reserve are engaged in the bailout of the private credit sector. Massive amounts of money (liquidity) are being pumped into the U.S. financial system through them, which shows in the relentless growth of the U.S. money supply.

Furthermore, there may be another hidden bailout occurring through the U.S. repo market.

The two statistical drivers of U.S. repo markets

In the April Black Swan Outlook, we took notice of the repo markets and the Federal Reserve concealing a “black swan” in the private credit sector, continuing the analyses by Tuomas.1 Here we aim to deepen our understanding of the statistical drivers of U.S. repo markets, as it will help us comprehend the nature of the stress involved. Bare with us.

Let’s start by looking at the rates of the Triparty General Collateral Rate (TGCR), the Secured Overnight Financing Rate (SOFR), the Broad General Collateral Rate (BGCR), and the Interest Rate on Reserve Balances (IORB). Figure 3 reveals three important observations on them.