Contents:

Developments in lending to the Private Credit.

Forecasts for U.S. business lending and lending to NDFIs.

This week we concentrate on Private Credit. Yesterday, I published an entry that detailed the “hidden” explosive growth of loans to the non-depository financial institutions, which consist mostly of credit funds and other “creatures” of the private credit sector. I actually came across the data while I was writing this.

What we uncover here are notably developments occurring in the lending of U.S. banks. We consider them to be symptoms of an ongoing bailout of the private credit sector by major U.S. banks.

Our forecasts present two paths ahead for U.S. bank lending. The other is more lenient, while the other presents a shock approaching the sector, which could lead to tighter lending standards and increased risk for borrowers. At this point, we cannot fully assess which is more reliable. The “shock model” has better statistical properties, but the scenario it paints is extreme.

Patricia will take a break from writing to us this week, while I report our recent email discussion later today. Another geopolitical expert will soon join us to write semi-regularly. I will introduce him when his first piece is published.

Have a great weekend!

Tuomas

Are there signs of cracks in lending to the U.S. private credit sector?

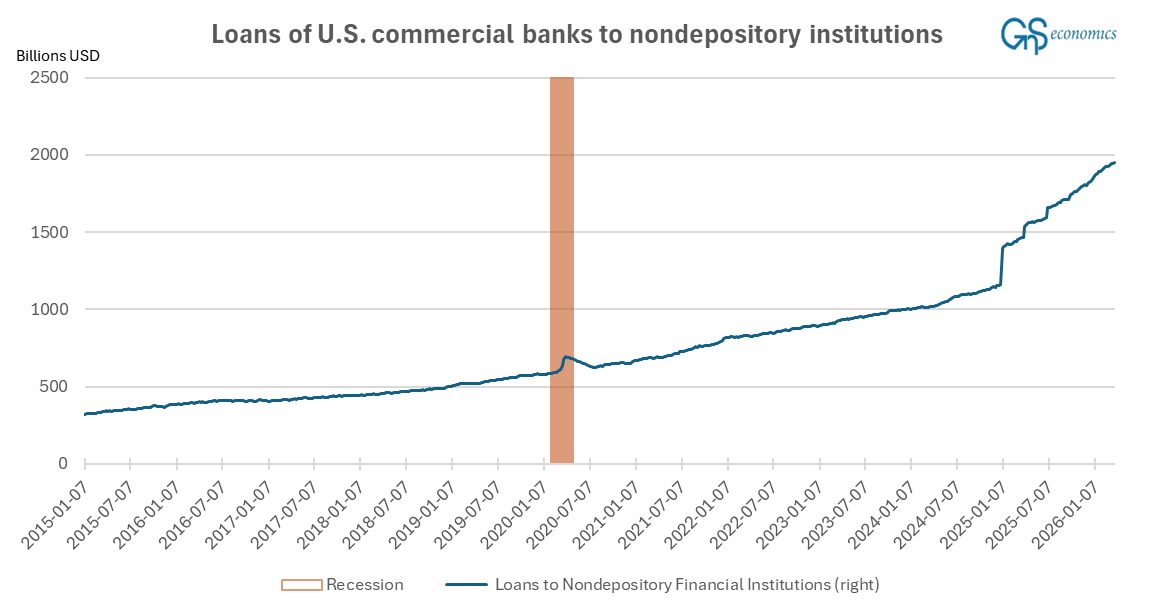

We start our analysis by assessing the recent developments in lending of U.S. commercial banks. They show clear developments or changes from our last comprehensive look at the sector at the end of November. Let’s begin by assessing the development of lending to non-depository institutions by U.S. commercial banks.1

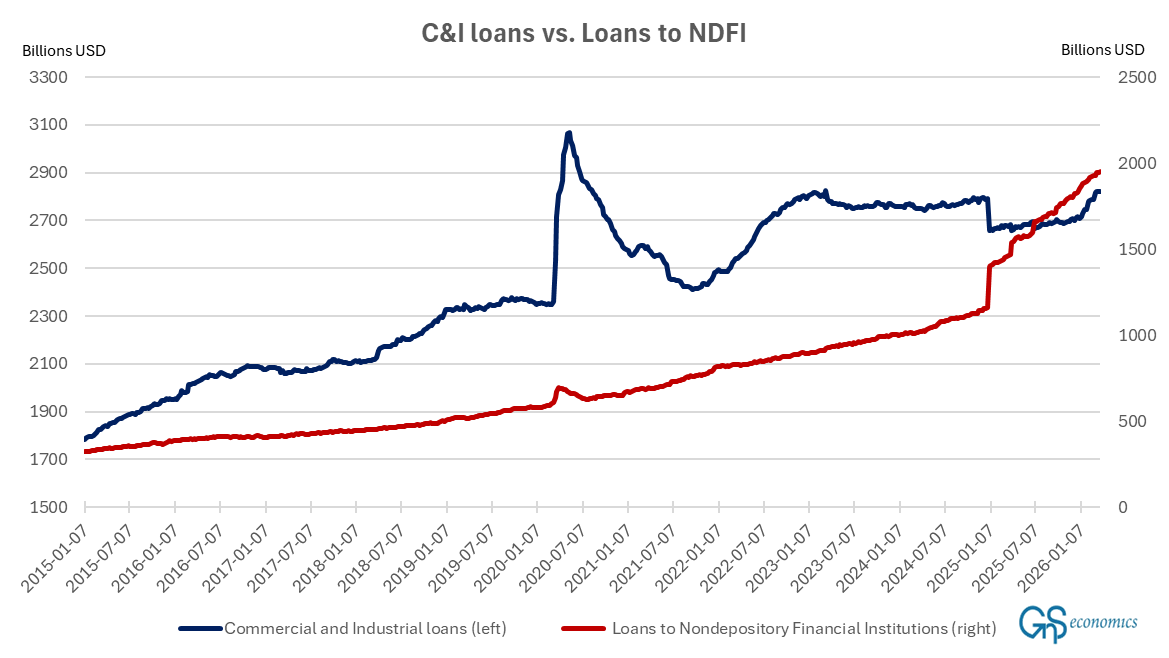

Lending by U.S. commercial banks to the NDFI’s has continued unabated since our last check in November. There has been a smallish slowing down in the lending activity during the recent weeks, but nothing drastic. However, business loans issued by U.S. banks reveal a very interesting recent development.

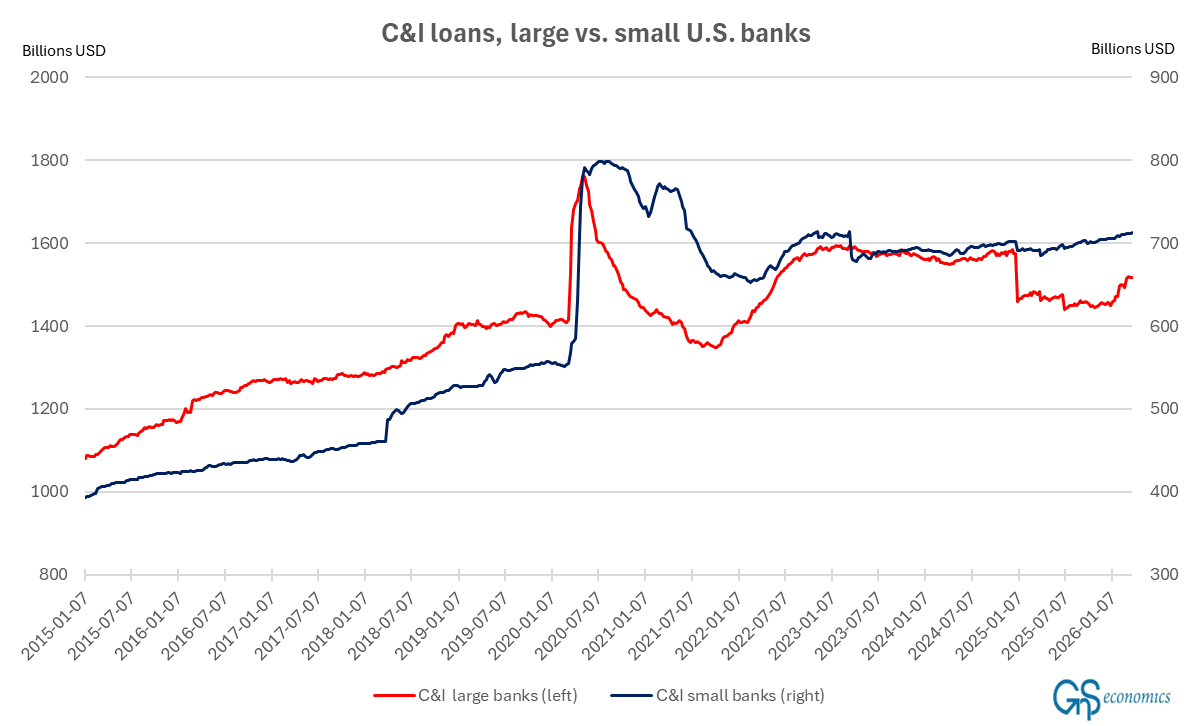

From late January on, the business lending activity of U.S. banks saw a massive increase in the magnitude we have not seen since June 2022 (when U.S. inflation peaked).2 This is interesting and could be speculated to indicate a notable pickup in business activity of U.S. companies. However, the devil is in the details also on this one. Figure 3 presents the split of business lending between large and small U.S. commercial banks.

Figure 3 shows that most of the growth in business lending has come from large U.S. banks, while the growth of the business lending of smaller banks has remained steady. If we were to expect a notable pick-up in U.S. business activity, we should see the business lending of smaller banks increase because they fund especially the local small- and mid-sized companies, SMEs, which are the backbone of the U.S. economy. We are not seeing this. So, what is going on?