Tuomas raised the issue that asset markets, and the economy, could follow the catastrophic path of 1929 in his recent post (see also this). We have now found more evidence to support this hypothesis, carrying a stark warning for the asset markets.

First of all, recession talk has been getting louder in recent days. For example, JP Morgan’s head of global fixed income, Bob Michele, warned on U.S. recession arriving “by the year end”, while Robert Heller, a former governor of the Fed, warned that U.S. recession is “absolutely possible”. Because central bankers, even after they’re retired, tend not to forecast onset of recessions, the warning of Dr. Heller carries weight. Also, the leading indicators of the Conference Board are pointing to a sharply slowing economic growth also by the year-end (see July Deprcon Outlook).

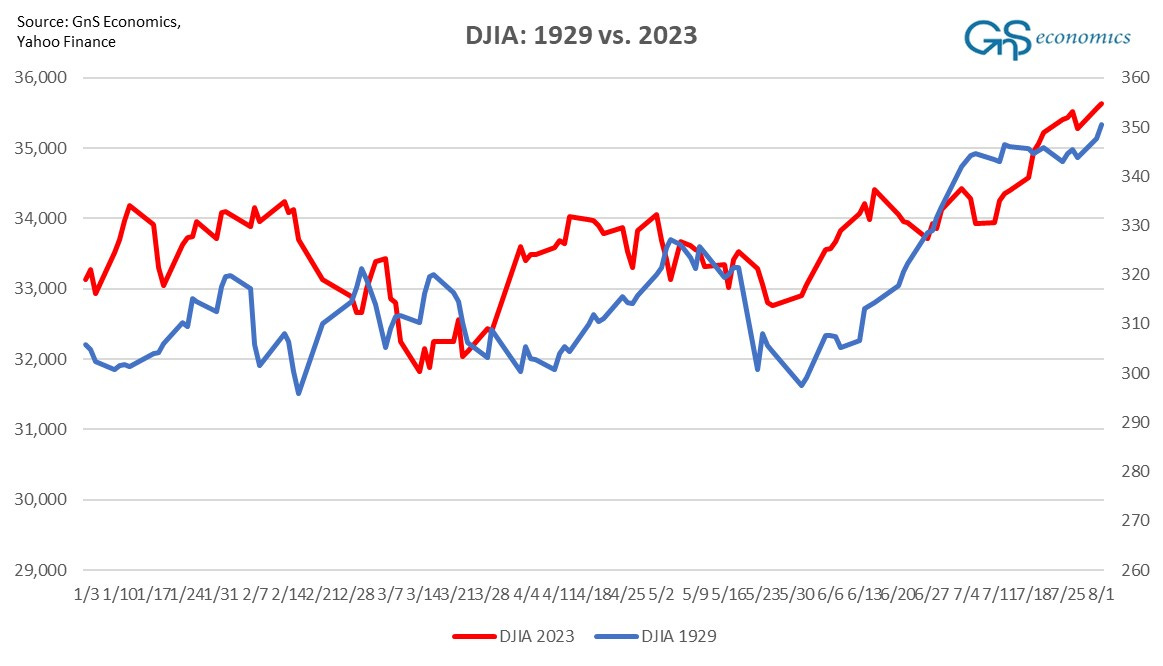

Relating to this, we found a worrying correlation in the historical patterns of stock markets. The recent ‘bull run’ in asset markets has followed that of 1929 with notable accuracy. The correlation of daily moves of the Dow Jones Industrial Average (DJIA) between 1929 and 2023 56%. This is a very high correlation for time series following stochastic processes (with time trends).1

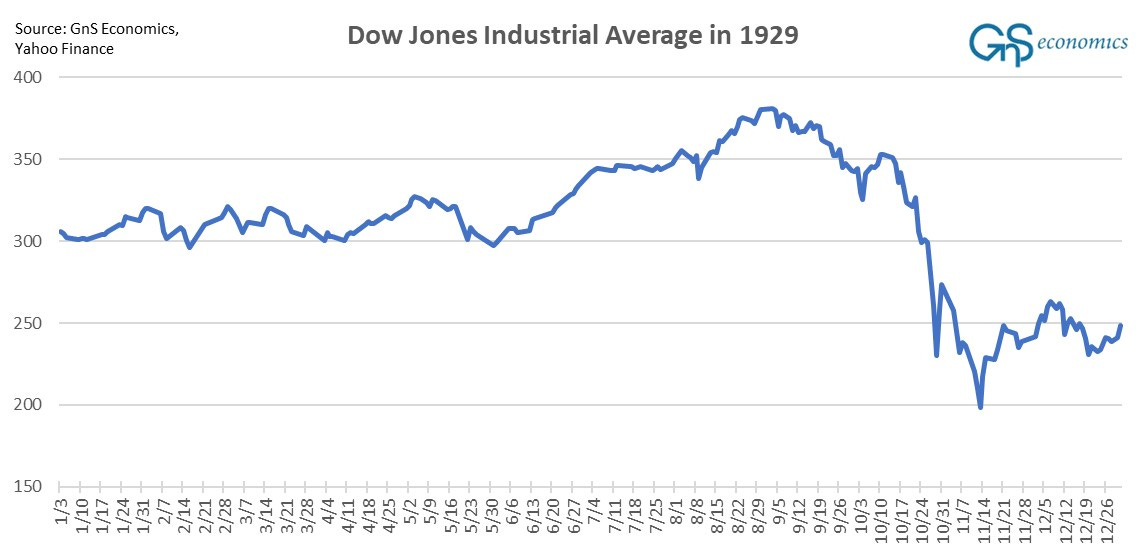

What happened to stock markets after August 1929, is the worrying part. In 1929, the first hints of a slowing economy came in July, when the index of industrial production of the Fed dropped (there were, e.g., no quarterly earnings reports). From then on, several other indices, including steel production and freight-car loads, started falling. The mix of bad news and rising interest rates foretold on upcoming recession, and the markets started to drift downwards in early September. Between 24-29 October, the U.S. stock markets crashed by 29%.

History rarely repeats itself, but it often rhymes. Recession signals are likely to grow louder from here on, and a precarious mood is likely to start to creep in the markets (if it hasn’t already).

If our forecast on the major liquidity drain in September/October holds true, we may face a souring investor sentiment, with recession signals growing louder, and a collapsing market liquidity. This would almost certainly lead to a crash, even without the possible (likely) resurfacing of the banking crisis.

We thus urge caution in all financial market activity during August, and especially in September and October. It’s important to note that, when the downturn in the asset markets appears, if can be a long journey to the bottom.

Disclaimer:

The information contained herein is current as at the date of this entry. The information presented here is considered reliable, but its accuracy is not guaranteed. Changes may occur in the circumstances after the date of this entry and the information contained in this post may not hold true in the future.

No information contained in this entry should be construed as investment advice. GnS Economics nor any of the authors cannot be held responsible for errors or omissions in the data presented. Readers should always consult their own personal financial or investment advisor before making any investment decision, and readers using this post do so solely at their own risk.

Readers must make an independent assessment of the risks involved and of the legal, tax, business, financial or other consequences of their actions. GnS Economics nor any of the authors cannot be held i) responsible for any decision taken, act or omission; or ii) liable for damages caused by such measures.

A more precise mathematical description for such a series is a random walk with drift. This means that the series moves randomly through time around some trend (positive or negative). While the concept of a random walk is somewhat debatable in academics still, the idea that shocks, considered random (unforecastable), drive the daily moves of the series can be considered plausible.