In this Outlook, we return to providing a deeper analysis of the U.S. banking sector. We start with an overall update on recent trends, which indicate a major increase in lending to the Private Credit sector. While aggregate-level data is not enough to confirm this, the loans to Non-Depository Financial Institutions give an indication that banks are increasingly funding the shadow banking system, where leverage and risk-taking have grown rapidly outside traditional oversight. This shift marks one of the most significant but least transparent credit trends in the post-pandemic era.

Before going into this, we provide the “usuals”, i.e., economic growth and China stimulus forecasts. We end with a (pre-)warning concerning the U.S. stock markets.

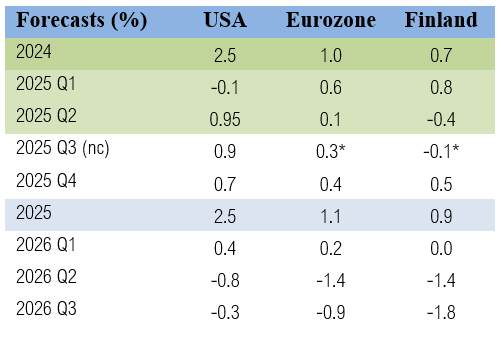

GDP Forecasts

The real gross domestic product (GDP) of the U.S. should have received an update and the first estimate for Q3 growth yesterday. However, the government shutdown delayed their publication until an unknown date. The Eurozone and Finland received their GDP updates on schedule. According to the first estimate, the Eurozone economy grew at a faster-than-expected rate of 0.3% quarter-to-quarter (1.3% year-over-year) in the third quarter. The Finnish economy shrank by 0.1% (Q-to-Q) during the third quarter. Our last nowcasts, at the end of September, were 0.2% and -0.1%, respectively. So, we missed the realized (first estimate) Q-to-Q growth of the economy of the Eurozone by meagre 0.1%, while we were right on the money on the deceleration of the Finnish economy. Our nowcasts indicate that the U.S. economy would have grown by 0.9% Q-to-Q during Q3 (3.6% year-over-year).

Naturally we were unable to update our forecasts for U.S. GDP, as there was no updated data. Thus, our forecasts for the U.S. continue to be based on our latest update from 26 September, which shows a sharp drop in the U.S. GDP during Q2 and Q3 next year. This forecast basically dominates the forecasts of the Eurozone and Finland, because the U.S. has a dominant role in our model (as in real-life). At this point, we thus cannot do more than just wait for the first estimate on U.S. GDP to gain more insight on the current economic situation and the way forward.

Forecasts for the stimulus of China

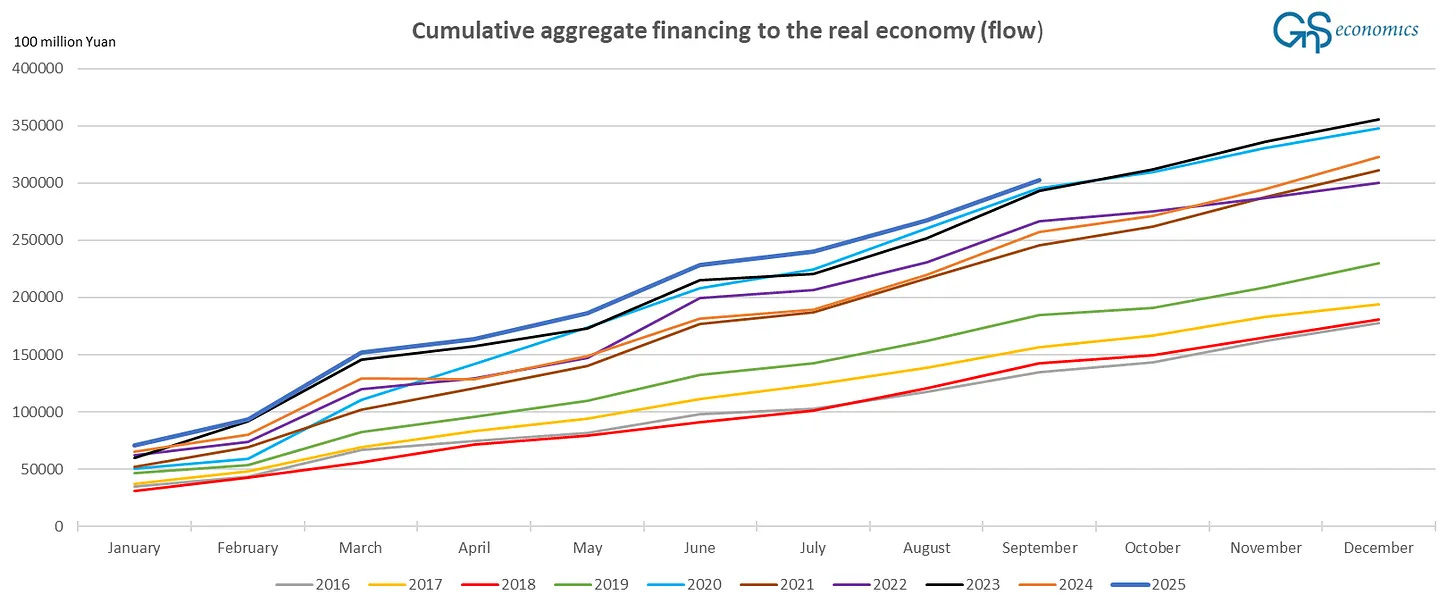

Push. The amount of money entering the Chinese economy grew by RMB3.53 trillion in September. This was the lowest September flow of financing since 2021. Although the last two months showed below-average monthly flows of financing into the Chinese economy, the total cumulative flow of aggregate financing is still on track to reach a new annual record, as we forecasted at the beginning of the year.

It thus now seems that A) either Beijing is confident that a trade truce will be found with the administration of President Trump, or that the trade war will not deliver a major hit to the Chinese economy after all, or B) Beijing is throwing in the towel when it comes to the economy, again. It is also possible that a combination of these factors is at play. We also consider that Beijing is well aware of the massive debt bubble it is presiding over and which it has created. Considering the above it is thus no surprise that the leading indicators of China have been heading down of late.

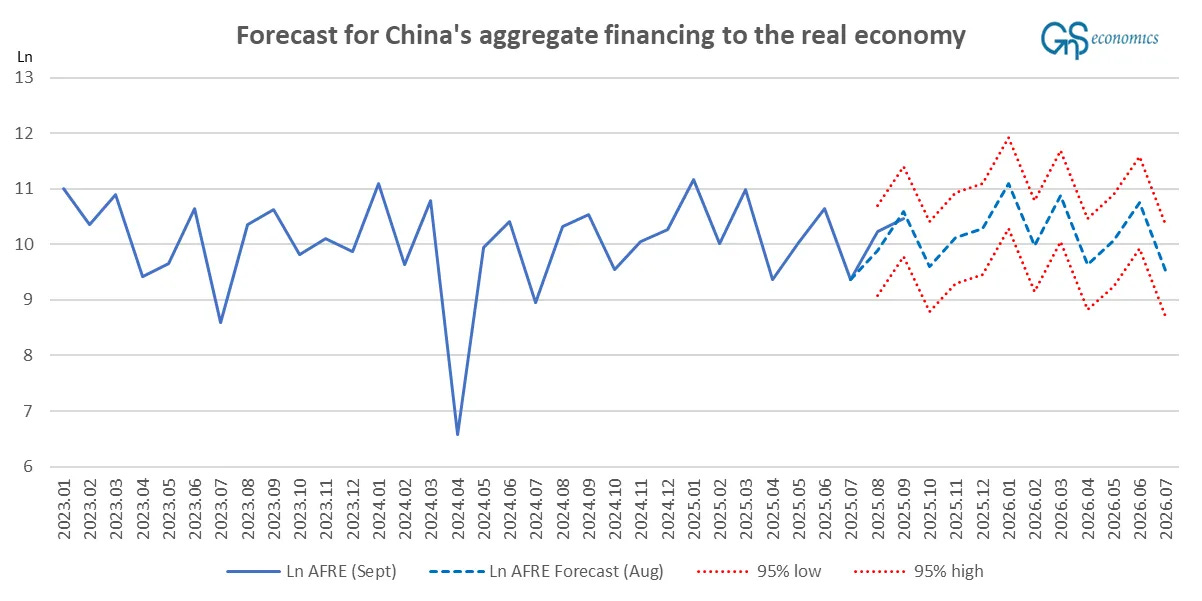

Our forecasting model for financing flows of the Chinese economy continues to shine. Figure 3 shows our forecasts from August (with data reaching July) vs. the actualized values of aggregate financing to the Chinese economy.

Keep reading with a 7-day free trial

Subscribe to GnS Economics Newsletter to keep reading this post and get 7 days of free access to the full post archives.