At a loss

Where is the money growth in the U.S. coming from? (Free)

From Tuomas Malinen on Geopolitics and the Economy.

I am, again, pondering why the M2 monetary aggregate is growing despite the quantitative tightening, that is, the asset roll-off of the Federal Reserve.1 The U.S. M2 hit a post-Corona bottom on 30 October 2023 and then started to grow without any apparent reason.

Quantitative tightening (QT) operates by selling the assets the Primary Dealers banks of the Federal Reserve have obtained back to the populace and corporations. Some economists still claim that quantitative easing (QE), i.e., the Fed buying assets, would not be money printing because the Fed is just conducting an “asset swap” and not creating “new money” into the economy. This claim is utter and total nonsense.

First of all, changing the allocation of assets within the central banks and thus the economy is how central banks can create money by, e.g., changing the reserves banks are required to hold, called “excess reserves”. Secondly, from my 2022 piece in the Epoch Times:

When a central bank buys assets through QE, it operates only through so-called Primary Dealer banks which, however, are not often banks but broker-dealers. The central bank buys the assets, usually Treasurys, with newly created central bank reserves, which are “excess reserves” to a bank. So the central bank doesn’t buy the assets with money, but with reserves, that is, deposits at the central bank.

If the seller is a bank, it ends up holding the excess reserves (in exchange for the assets). However, if the seller of the asset is a non-bank, for example, a corporation, hedge fund, pension fund, or another trader, the reserves end up going to the central bank account of the bank of the non-bank. These will be balanced with new deposits, which are owed to the non-bank. That is, assets are bought from non-banks with deposits.

[…]

Seth Carpenter, Selva Demiralp, Jane Ihrig, and Elizabeth Klee found in their paper, “Analyzing Federal Reserve asset purchases: From whom does the Fed buy?” that, during QE1 and QE2 which ran between November 2008 and December 2012, the Fed bought Treasuries mostly from households, including hedge funds and pension funds. Essentially what happened during Q1 and Q2 was that the Fed pushed vast amounts of cash assets into commercial banks. When the Fed has shrunk its balance sheet by selling the assets, in a program called quantitative tightening (QT), the opposite has happened.

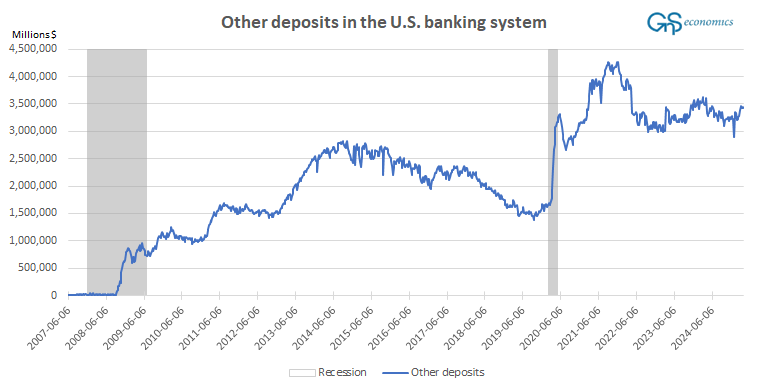

The QE programs were de facto money printing, which is why QT programs are, effectively, money destruction. These manifest themselves through the deposits banks hold at the Fed. These balances (see the figure below) should rise with QE, as central banks force more reserves into the banks, and decline with QT, as reserves in the banking system decrease.

The Fed started its QT in June 2022, but the reserves started to dwindle already in early 2022. This is because the reserves tend to “leak” out through, e.g., the repo-market.2 Banks can use excess reserves (reserves above the minimum limit) as collateral in the repo-markets to obtain short-term liquidity. Banks can roll-over these contracts by (constantly) renewing these short-term contracts, effectively creating money in the system.

The strange thing is that the Other deposits, which reflect the excess reserves banks hold at the Fed, stopped their decline in October 2022. Moreover, at the beginning of February, the excess reserves turned back to growth. This implies that banks are returning the reserves from the repo operations in a search for safe assets/security. This should lead to a decline in the money supply within the economy. Yet, the absolute opposite is occurring. The M2 has accelerated its ascent since the beginning of February. This would make sense if lending by U.S. banks were growing rapidly, but it’s not.

So, why is M2 growing when the balance sheet of the Fed is declining and the lending of U.S. commercial banks is growing at a subpar level?

One source is the reverse repo facility of the Fed, where banks have been “parking” money overnight. Those balances are now reaching zero, but they cannot explain the recent uptick in the M2 money because most of that “excess money” was depleted by the end of last year. The other thing is that demand deposits are growing rapidly again, but banks are not lending this out but demanding more reserves (at least this is how it looks from above). This should show as a declining, or at least stagnating, growth of money, but the opposite is happening.

I have to admit that I am at a loss here,

Tuomas

Disclaimer:

The information contained herein is current as of the date of this entry. The information presented here is considered reliable, but its accuracy is not guaranteed. Changes may occur in the circumstances after the date of this entry, and the information contained in this post may not hold true in the future.

No information contained in this entry should be construed as investment advice nor advice on the safety of banks. GnS Economics, any of its partners and employees, nor Tuomas Malinen cannot be held responsible for errors or omissions in the data presented. Readers should always consult their own personal financial or investment advisor before making any investment decision or decision on banks they hold their money in. Readers using this post do so solely at their own risk.

Readers must make an independent assessment of the risks involved and of the legal, tax, business, financial, or other consequences of their actions. GnS Economics nor Tuomas Malinen or any other authors cannot be held i) responsible for any decision taken, act or omission; or ii) liable for damages caused by such measures.

I wish to thank Dr. Peter Nyberg for comments and suggestions. Remaining errors are my own.

The repurchase agreement, or “repo”, is a financial agreement in which the borrower agrees to buy back the security it sold to the lender at a later date for a higher price. A repurchase agreement is essentially a short-term loan backed by high-quality collateral, most often 10-year Treasury bonds.

Repo agreement is essentially a financial agreement in which the borrower agrees to buy back the security it sold to the lender at a later date for a higher price. In a reverse repo contract, which is the repo contract from the lender’s perspective, the investor buys collateral in the form of fixed-income assets.

The reverse repo contract, which is the repo contract from the lender’s perspective, can also be used to invest cash. In a reverse repo, the investor buys collateral in the form of fixed-income assets.