Weekly Forecasts 4/2026

Inbound global recession and looming chaos in the Middle East

Contents:

GDP growth forecasts.

Why President Trump seems so keen of making a (likely catastrophic) mistake in the Middle East?

Are OECD’s leading indicators signaling a turn into a global downturn and towards a recession?

Probably everyone who dares is currently waiting in anxiety for what President Trump will decide to do in the Middle East. I consider that his “Armada” is there more just as a show of force than to start on actual war, but it is becoming more and more difficult for him to simply walk away each passing day. The situation appears chaotic, and decisions to strike vs. not strike can come and go in a whisk (we may have been in such a setup for a while already).

In this week’s forecasts, we explain the background of the current campaign against Iran. There is unlikely to be any single reason for the aggression, but rather a complex geopolitical “maze.” We consider that it involves the petrodollar trade and the threat of China, as well as aspirations arising from the main ally of the U.S. in the region, i.e., Israel.

We also update our forecasts for the GDP growth and encipher the recent signals of the leading indicators of the OECD through statistical analysis and forecasting. The main message of our economic forecasts continues to be that a downturn is approaching.

Tuomas

GDP growth forecasts

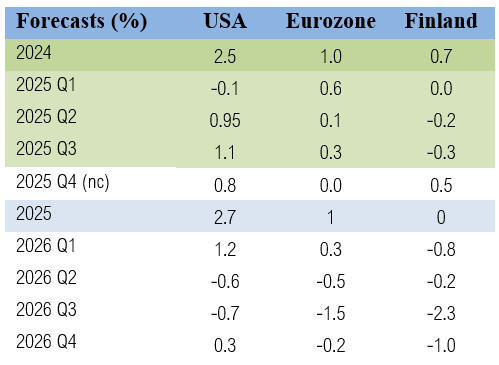

This is how our last forecasts for Q4 GDP growth looked like at the end of December. We were expecting the U.S. GDP to have grown at a 0.8% rate quarter-to-quarter, 3.2% annualized, and the Finnish GDP at a rate of 0.5% (Q-to-Q). Our forecasts expected the Eurozone economy would have stagnated.

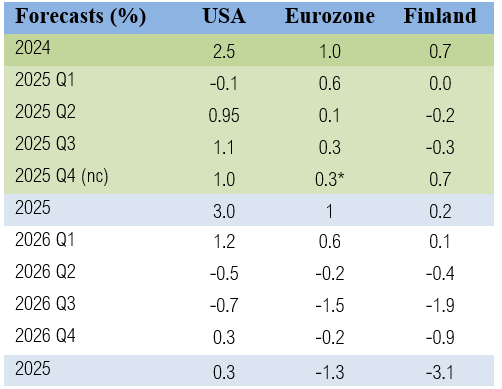

We will only get the first estimate for the growth of U.S. Q4 GDP in February, like that of Finland’s. Today, Eurostat published the first estimate for the growth rate of the Eurozone for Q4, which was 0.3%. Our last estimate from December was 0%, so we missed big to the downside. Here are our latest GDP growth forecasts.

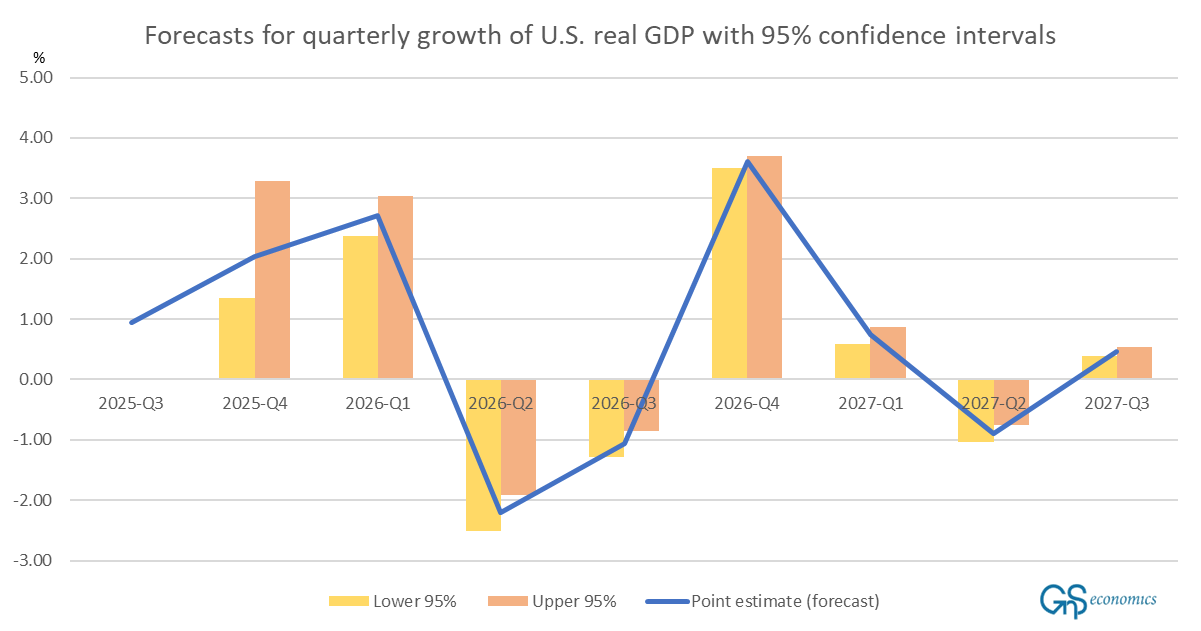

Our nowcasts (with data reaching to the end of December) are now indicating that both the U.S. and Finnish economies would have accelerated notably during Q4. In accordance with our forecasting model (see below), we are forecasting that the acceleration of the U.S. will continue during this quarter but then hit a wall in Q2. We forecast the Eurozone economy to also pick up pace during this quarter before entering into a slump in Q2. We have to note that the Q2-Q3 decline in the growth rates is driven fully by our medium-term forecasting model for the U.S. and by our forecasts for OECD’s leading indicators presented below. Both of these forecasts include a heavy dose of uncertainty. Moreover, there are no shortages of potential shocks, one of which we list below. Every growth forecast for this year thus needs to be taken with a heavy grain of salt.

Our medium-term forecasting model thus keeps on anticipating the U.S. economy to pick up speed before crashing during the next two quarters. This result continues to baffle us, but as Tuomas has discussed this extensively during the past week (see, e.g., this and this), we do not comment on the result any further here. Let’s wait and see what comes.

Chaos looms in the Middle East, but why?

As of the time of writing, the situation around Iran looks precarious. There are no clear indications that U.S.-Israel strikes on Iran would be imminent, but the pressure is building. Tuomas has warned of the implications of such catastrophic escalation several times in recent weeks. Here we detail some Iranian capabilities affecting the decisions of President Trump and offer some conjecture as to why the U.S.-Israel axis seems so hellbent to deliver a regime change in Iran.