Weekly Forecasts 13/2025

Delinquencies everywhere

Forecasts:

U.S. bank loan trends overview.

Is there a new problem in the house?

Another recession warning for the U.S. triggered and projection of non-performing loans.

A quick recap

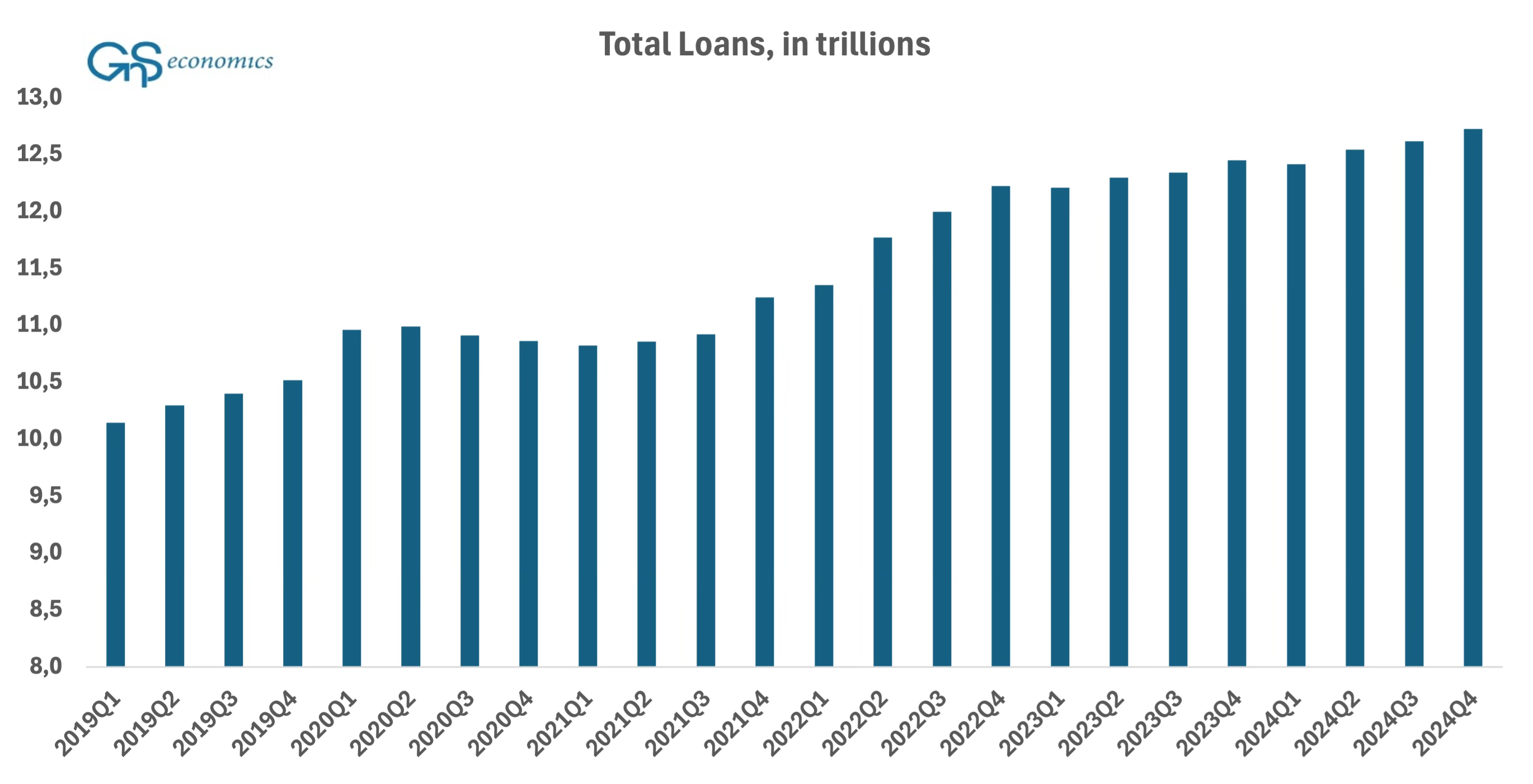

Under the QT (quantitative tightening) and risk-off environment, U.S. banks are barely growing their loan portfolios, which is expected, but at least it is still on an upward trajectory. The combined loan portfolio of U.S. banks is standing at 12.73 trillion dollars, per the 24Q4 FDIC (Federal Deposit Insurance Company) filing, growing at an average of 0.1 trillion by quarter since the start of rate hiking in March 2022.

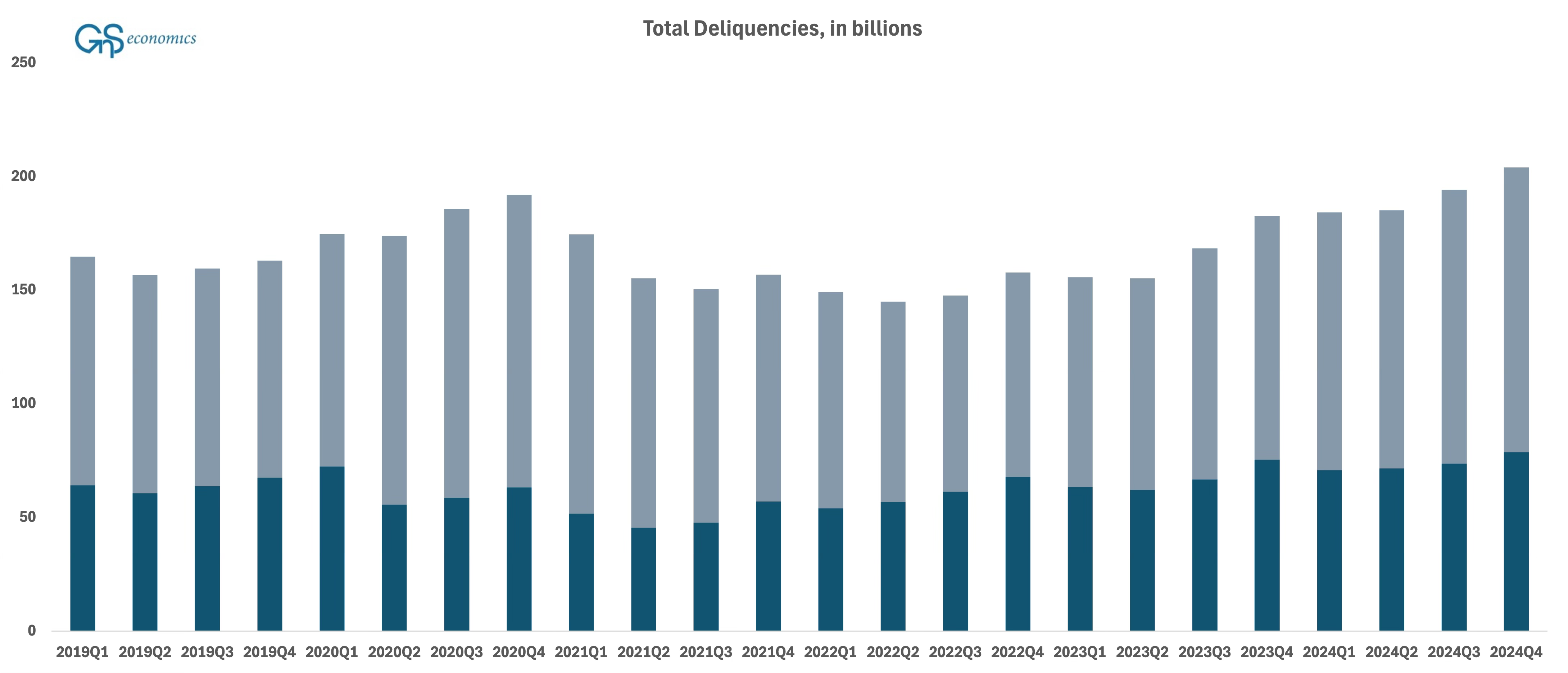

Unsurprisingly, under the hood, the issues are still brewing, which causes U.S. banks to think twice before taking on more loans. Every quarter, delinquencies are steadily increasing, not to such an extent as to cause significant problems, but it is still a matter worth keeping an eye on. Early-stage (30-89 days) loans alongside with non-performing loans (NPL) are standing close to 200 billion after rising for seven consecutive quarters.

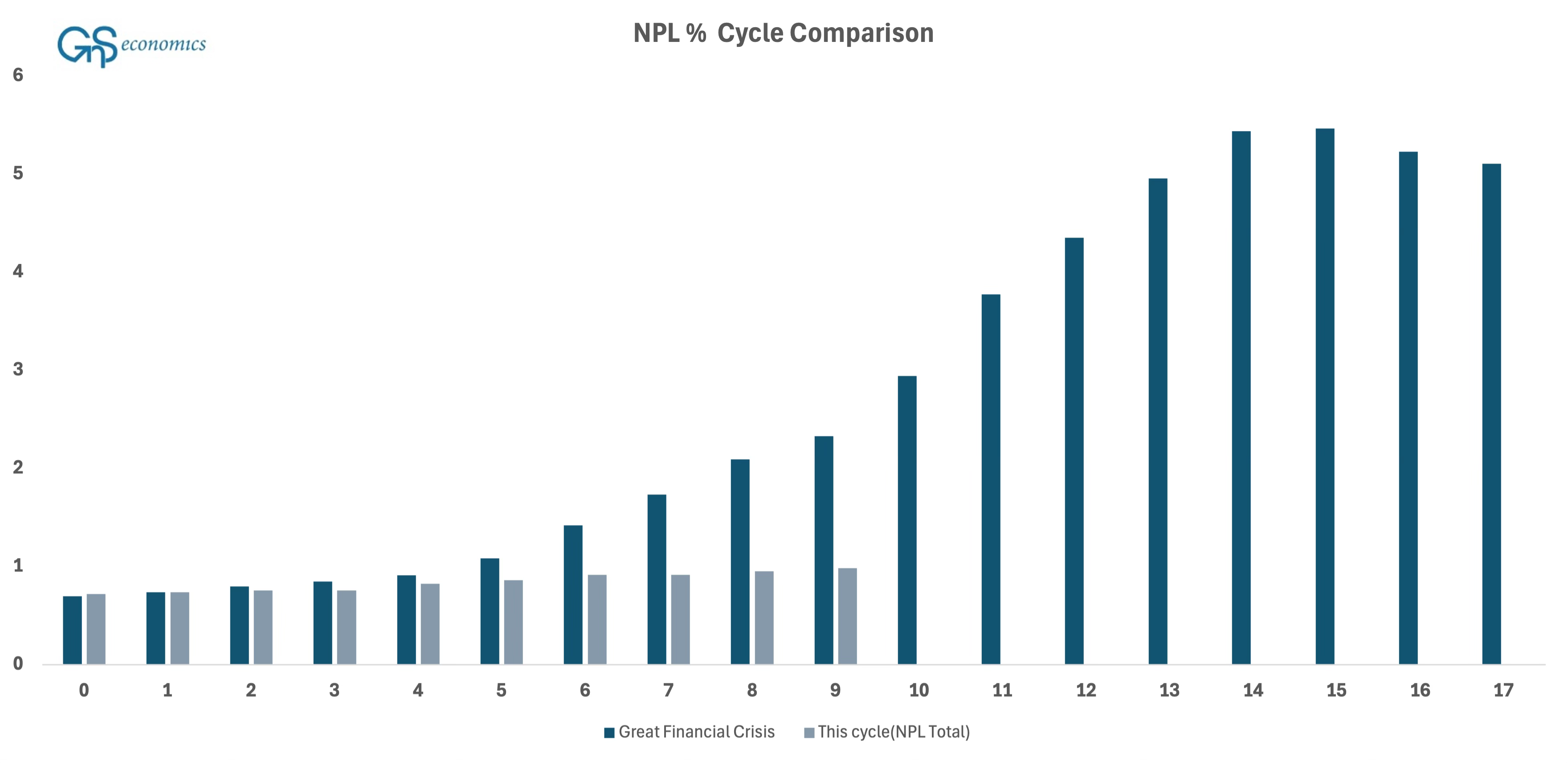

On the bright side, comparing the trajectory of the overall NPL ratio during recent quarters and during the Great Financial Crisis (GFC) shows us a consolidating picture. We can clearly see how much more aggressive the NPL growth was in the GFC, while this time it has stayed under control, for now at least.

Weak Spots

Keep reading with a 7-day free trial

Subscribe to GnS Economics Newsletter to keep reading this post and get 7 days of free access to the full post archives.