The Recession Conundrum

The "battle" between traditional metrics vs. forecasts of GnS Economics

We have entered a conundrum with our economic outlook. I will now present to you three highly differing measures of the U.S. economy (well, the latter is also global). Let’s start with something I and we at GnS Economics have been following for many years, the yield curve.

We have concentrated on the spreads of U.S. Treasuries with 10-year/3-month and 10-year/2-year maturities because they have been shown to have the best recession forecasting ability by academic research and real-life experience. You see the latter in this figure.

In What about dat recession, I noted:

The (historical) fact is that every time the 10y/2y yield curve has reached this level, recovering from an inversion, the U.S. economy has either been in a recession already or then its onset has been just three months away.

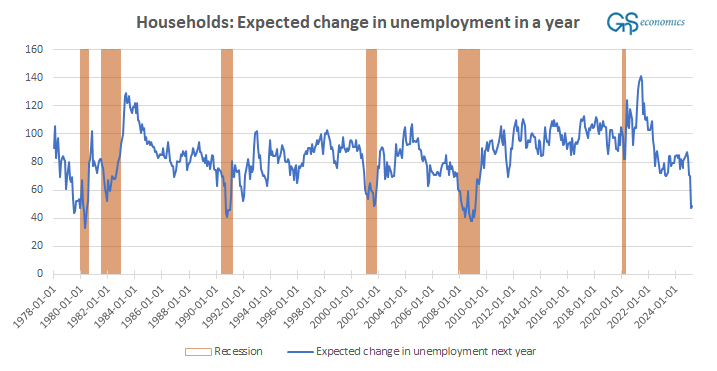

The case for the near-imminent onset of U.S. recession thus seems clear. Moreover, the expectations of U.S. households concerning their job prospects continue to be abysmal.

The expectations of U.S. households on their unemployment situation during the next 12 months continue to hover at levels last seen during the spring of 2009, i.e., near the bottom of the Great Financial Crisis. From the above, we would need to conclude that the U.S. should be heading into a recession. Yet, two recent forecasts from GnS Economics stand against this economic bleakness.

Keep reading with a 7-day free trial

Subscribe to GnS Economics Newsletter to keep reading this post and get 7 days of free access to the full post archives.