Next round of U.S. Bank Runs Loom

This is not looking good...

From Tuomas Malinen on Geopolitics and the Economy.

I observed a worrying development, which I will report shortly here (I am working through the Christmas this year). In early November, I published a warning on yet another deterioration on the quality of the regulatory capital of U.S. banks. The prior deterioration preceded the March 2023 U.S. bank runs.

I commented this development by noting that:

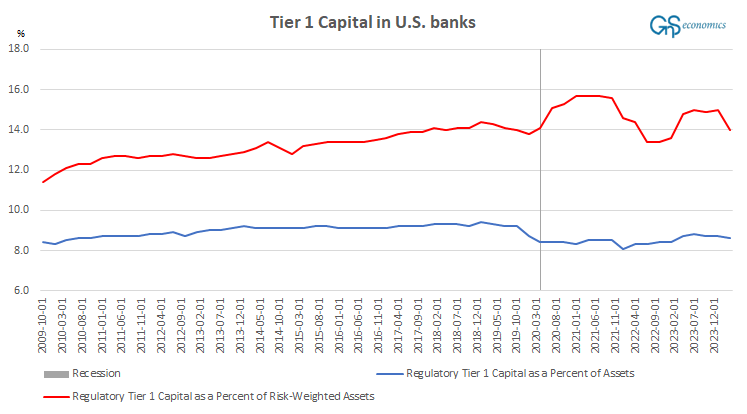

Now, we do not have a massive QE -program forcing excess reserves into banks, and the share of Tier 1 capital to assets is rather stable, but something is definitely happening to the risk-weighted assets. That is, the figure implies that they are deteriorating, again.

We naturally do not know the exact nature and composition of assets in U.S. banks, so we can only speculate. However, loans are the biggest asset category for commercial banks, which means that any changes in their riskiness will move the risk-weights of banks. As the Tier 1 capital ratio to risky-weighted assets is declining, this implies that the riskiness of loans in the balance sheets of banks is increasing. What could be the reason?

Now, we also have this.

Keep reading with a 7-day free trial

Subscribe to GnS Economics Newsletter to keep reading this post and get 7 days of free access to the full post archives.