From Tuomas Malinen’s Forecasting Newsletter.

Issues discussed:

China has carried the world economy since 2009.

China’s economic model is effectively broken (“maxed out”), which has some dire implications for the world economy.

The global ‘Minsky moment’, I warned on in August, is likely to be upon us (or we are very close).

On Wednesday, GnS Economics issued a warning on the state of the U.S. banking sector I urge you to check it.

The economic doom-and-gloom touted by me, and by GnS Economics, has but one origin: China. I think I’ve told this story before, but our dark view arose from the wilderness of western Lapland. Me and my ex-wife had a habit of spending the New Year in a small resort village near Pallastunturi. We hiked in the fell, went skiing, “hunted” for Northern Lights and just enjoyed the calmness and beauty of the Polar Night.

In late 2016, we were there again, and my ex-wife was reading Thinking Fast and Slow by Daniel Kahneman. The book deals with human decision making and especially rational and non-rational motivations, or triggers, associated with human decisions. One of the subtopics of the book are errors in forecasting. We started talking about our forecasts and I told her that “I think that something is seriously off with the world economy, and our forecasts”. This was because the world economy had slowed notably in 2015 only to shoot up from the brink of a recession a year after without any clear explanation. She replied by asking that am I sure that I am not simply following my previous (erroneous) thinking, or “Inside view”, as described by Dr. Kahneman. This got me thinking, and when we got home, I thrashed all the data and models we had been using, and started over.

Three months later, we published our first “doom-and-gloom” quarterly report, Bellwethers of a Fall, where we issued our first-ever warning of a global crash. I had discovered that the world economy had never truly recovered from the Great Financial Crisis of 2007-2008. Everything in the financial markets had just become supported by the central banks, depicted in the figure below (straight from the report). However, while it was apparent that central banks saved the financial markets, it left me wondering who had resuscitated the world economy?

Enter the dragon

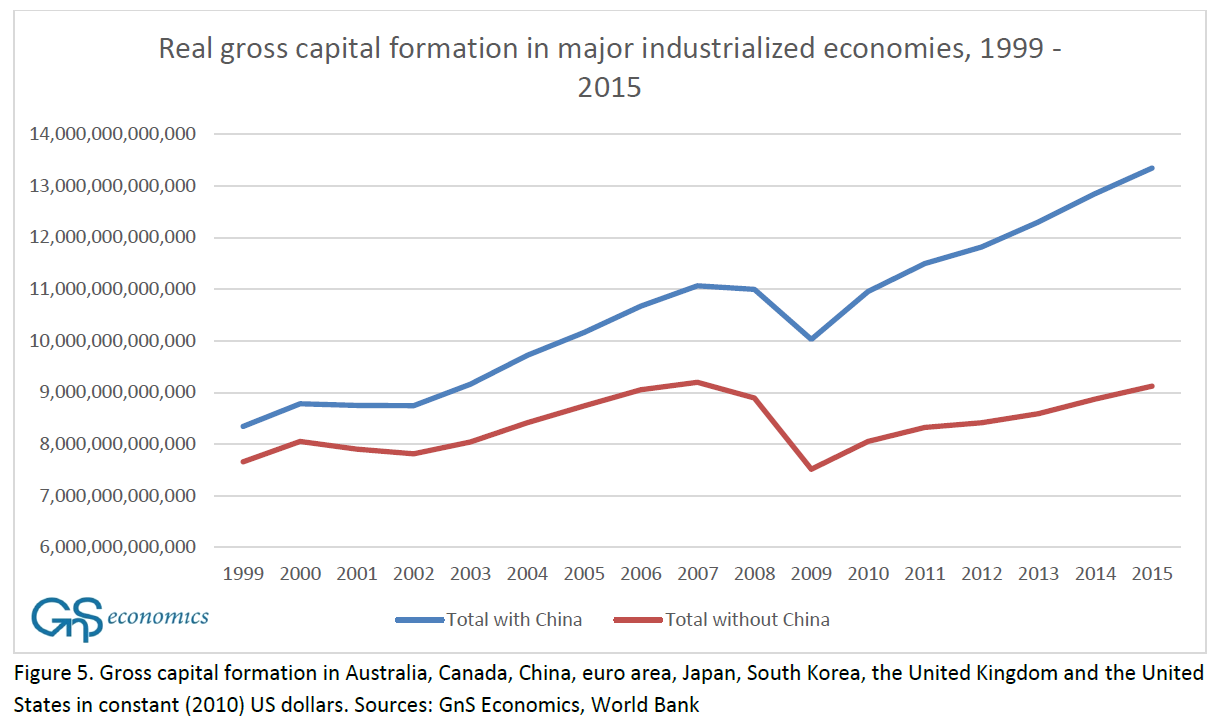

The answer presented itself during the following summer. After another round of excessive “data-mining”, I learned that China had rescued the world economy in 2009 with massive debt stimulus. We published my findings in a report entitled: The World Economy on the Brink. Most notably, China had been responsible for almost all creation of private debt in the world and most of capital investments since 2009 (figures are straight from the report).

Still, one thing bugged me. As there was no sudden spike visible in the debt statistics of China, where had the money for the stimulus and rapid acceleration of economic growth come from?

I kept on digging and found the answer in early 2018. It was published in March 2018, as a part of our special report on quantitative easing/tightening (asset purchase/roll-off) programs of central banks. The next figure depicts the reason why the world economy recovered so rapidly in 2016 “without a trace”.

In 2015/2016, China had run a gargantuan stimulus program financed through the shadow banking sector. “Shadow banking sector” is just a fancy name for financial corporations providing lending to corporations and local governments outside the traditional, regulated banking sector. In just one year (2016), the balance sheet of shadow banks grew from around $12 trillion to over $38 trillion. This means that in just one year, China’s banking sector grew into a bloated behemoth. The unsustainability of the credit binge became painfully obvious, when we compared the size of the banking sector of China to that of the U.S. right before it collapsed in the Great Financial Crisis.

The dominating role China has held on the world economy since 2009 (see also this) makes her current economic woes very worrying. As we warned in October 2017:

If the asset value destruction starts, and the “jump” happens in China, it will be followed by debt destruction or deflation. Because China has been responsible for over 95 % of global private debt creation since 2008 (see the figure below), global private debt will start to contract (unless other large economies and corporations commence a massive investment spree, which is unlikely). This China-induced global debt deflation will mean a global asset deflation, and thus a global ‘Minsky moment’. So, if China faces a Minsky moment, the world, with high probability, will face it also.

Everything that is now manifesting in China is related 1) to her major debt stimulus ran from 2009 on, and 2) to the gargantuan credit binge enacted through the shadow banking sector in 2016. (More on the Minsky moment below.)

Let’s now take a closer look of how bad the situation in China currently is.

Exit the dragon

Keep reading with a 7-day free trial

Subscribe to GnS Economics Newsletter to keep reading this post and get 7 days of free access to the full post archives.