Bellwethers of a Fall

The 2024 edition (free)

From Tuomas Malinen’s Forecasting Newsletter.

Global financial system has recovered from the Great Financial Crisis, somewhat, during the past few years.

The world economy has not.

Several developments threaten to de-rail the “recovery” (there’s no such thing; just more utterly unsustainable debt-stimulus).

In this entry I am going to take a walk down the memory lane. In March 2017, GnS Economics published a warning of a global crash in a piece entitled Bellwethers of a fall. In it we noted that:

To summarize, it is our view that the bubble in the world economy has just come too big to avoid a massive correction. Without some kind of “divine intervention”, the bubble will burst and the world economy will crash. We just do not know the exact date of its demise. The first signals of the bursting of the bubble could include increasing fluctuations (mini crashes) in the asset markets and stress on the money markets, especially in the inter-bank markets.

And that:

How long can this all continue? The simple answer is: As long as governments and central banks can keep it going. World economy has been supported by China recently, so a lot depends on what kind of a policy China takes. The asset purchases of the central banks will be limited by the assets available. The ability of central banks to act in a crisis is also questionable as they would suffer crippling losses if bond markets crash.

As we now know, governments and central bankers have ‘kept it going’, thus far. Here I am going to update the crucial figures behind our warning to see, where we stand now. I also provide clues to help you to forecast the important short-term developments, ranging from a likely liquidity withdrawal to Houthis

The situation in 2017

I am going to update these three figures with comments (without trend estimations). The three figures below are as presented in the report.

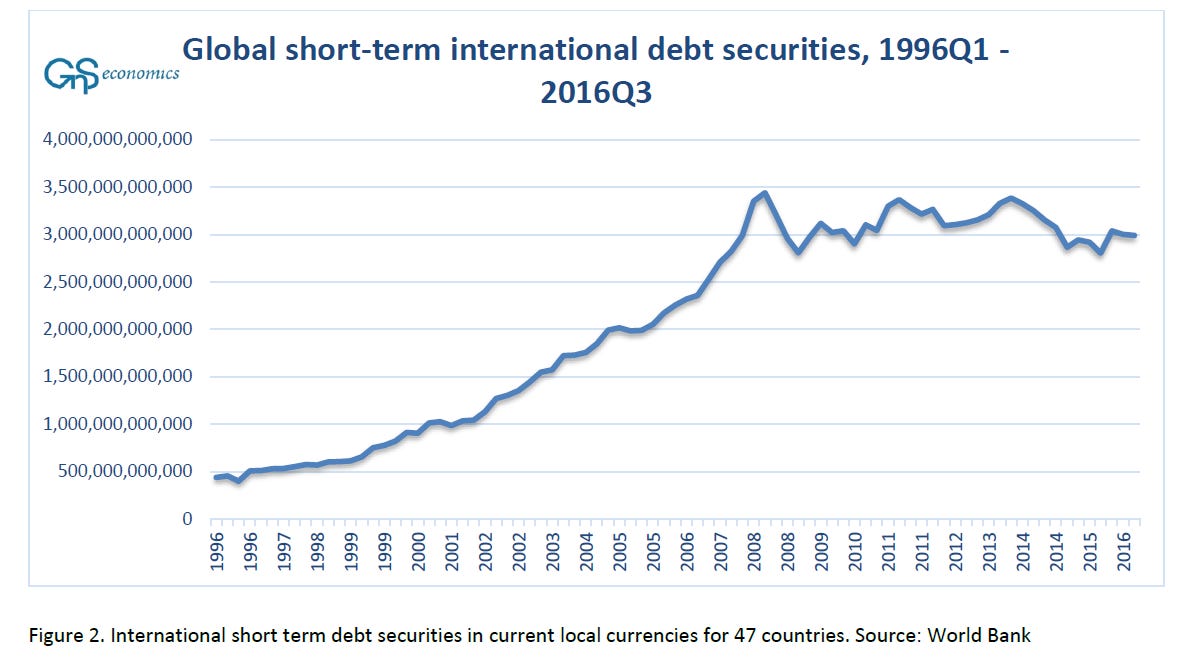

In March 2017, we argued that the data implied that there had been a reversal of financial globalization. This was visible in both stalling (and even declining) issuance of international debt securities and cross-currency loans of banks. This had forced central banks to step in with their QE programs to provide massive amounts of (artificial) liquidity to prop up the global financial markets (see the figure below).

What we did not know back then, however, was that after a financial crisis, it generally takes around 8 years for the financial system to recover. This was a result of a research by Kenneth Rogoff and Carmen Reinhart, which I had simply missed back then. So, what is the situation now, 15 years after the Great Financial Crisis (GFC)? Has there been a recovery?

The situation in 2023

Yes and no. The issuance of debt securities in international markets has recovered, but the same cannot really be said on cross-border foreign currency (FCY=foreign currency unit) lending between banks.

The international debt issuance has been on a clear upward trajectory since late 2018, but while international vis-a-vis bank lending has risen from its deep slump in 2017-2019, it’s far from reaching the levels seen before the GFC. It thus looks that the result of KR and CR stating that a recovery of a financial system from a criss takes about 8 years, seems to hold, partially, also this time around. However…

If we look at global money (credit) creation, it’s still utterly dominated by China. And, like I have explained before, China’s economy has been in a state of (slow-motion) collapse for months. Beijing has enacted draconian debt stimulus, yet again, but it will provide just a temporary relief.

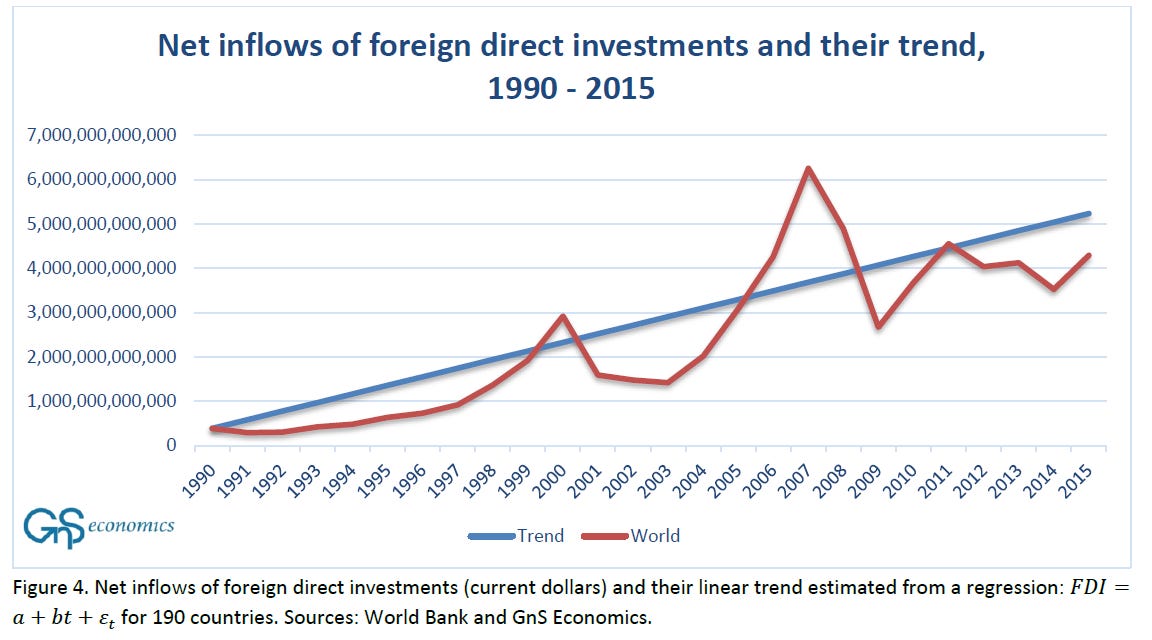

The last updated figure from the 2017 report shows that foreign investment inflows (into countries) have not recovered anywhere near the peak they reached in 2007. This enforces the view that global economy has never actually recovered from the GFC.

Conclusions

By comparing the 2017 and 2023 figures, we can conclude that while international debt issuance has recovered from the GFC, banking sector and global capital flows have not. Alas, the world economy has not fully recovered from the 2008 shock. The main reason why markets have rallied throughout this period (basically from 2009 on) is this.

Central banks have pumped massive amounts of liquidity (new money) into the markets since 2008. The ongoing programs of quantitative tightening (QT) have diminished the balance sheets of major central banks, but markets have held up due to strong injections of liquidity into the system by other means. Now, comments of tapering (of the QT programs) by board members of the ECB and regional Fed Presidents have already appeared most likely due to worries I shortly list below.

The world economy is currently experiencing a bounce, which we anticipated in the February Deprcon Outlook. The interesting thing is to learn, for how long Beijing will continue the currently-ongoing gargantuan debt stimulus and will there be an April liquidity-draining? I consider it very likely that at least the Biden administration will keep the major fiscal stimulus rolling till November, but Beijing could ‘succumb’ already earlier.

What comes to short-term forecasting, I urge you to keep an eye on these:

Volatility. If it starts to increase notably during, e.g., next week and the first week of April, it’s a likely sign of a liquidity draining commencing, which would lead to a downdraft in the markets in April.

The Fed speak. I am assuming that the urge to stop QT programs starts to weigh. This is because A) of uncertainty on what amounts of reserves the banking system needs to function properly, and B) because of the reverse repo facility of the Fed is about to run empty. When this pool of “excess money” runs out, it can create instability in the financial system.

Inflation. There are hints that inflation could pick up even further going into the summer. Food inflation and energy prices, as well as prices paid (and asked by) small and medium-sized companies tend to be good signals on where inflation is heading.

Warmongering. This is the most dangerous development currently. Western leaders are throwing ‘verbal-jabs’ to Russia and President Putin, by e.g., threatening to deploy western troops to Ukraine and by painting Russia as a threat to the “democratic world”. Such a harshening rhetoric can “accidentally” set WWIII ablaze by causing some party to act hastily. World War III is, by far, the biggest tail-risk at the moment.

Houthis and Israel. I just saw a piece in X arguing that Houthis have a super-sonic missile. That would pose a whole another level of threat to all Western assets in the region. Moreover, Benjamin Netanyahu has said that Israeli Defense Forces need to launch an operation to Rafah, a city in the border with Egypt, hosting half of the 2.3 million population of Gaza as refugees. An attack there would, most likely, increase tensions massively and it would carry the potential to set in motion my 10-point worst-case scenario.

Disclaimer:

The information contained herein is current as at the date of this entry. The information presented here is considered reliable, but its accuracy is not guaranteed. Changes may occur in the circumstances after the date of this entry and the information contained in this post may not hold true in the future.

No information contained in this entry should be construed as investment advice. GnS Economics nor Tuomas Malinen cannot be held responsible for errors or omissions in the data presented. Readers should always consult their own personal financial or investment advisor before making any investment decision, and readers using this post do so solely at their own risk.

Readers must make an independent assessment of the risks involved and of the legal, tax, business, financial or other consequences of their actions. GnS Economics nor Tuomas Malinen cannot be held i) responsible for any decision taken, act or omission; or ii) liable for damages caused by such measures.

I will deal with the reserve issue in more detail later, but there’s a level of central bank reserves required for the banking system to operate without problems. This is because central bank reserves are used by commercial banks to balance payments between them.

Major western "leaders" are in China's pocket, the Corona shut-down was a pilot program to see how the world economic system would react and to identify weaknesses and leverage points. China has been driving the world economy for the last 25 yrs and these disputes (Ukraine, Gaza) you write about are merely chess moves or enablers, as are digital currencies, AI, etc towards "Manifest Destiny 2030" eastern version. Given that this is the game that is underway, I find your drip feeding snippits of the moves being made without referencing macro strategy increasingly irritating.