World Economic Outlook

World Economic Outlook

September: Towards the Abyss

In this Outlook we continue to concentrate on the approaching recession in the U.S. and growing geopolitical tensions. The path we are on, implies that we are heading into some heavily disruptive events.

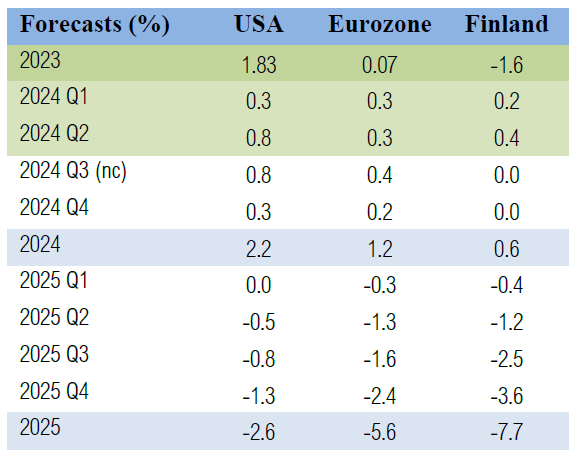

GDP Forecasts

(GnS Economics, OECD, Atlanta Fed, Statistics Finland, Q-to-Q). Our nowcasts indicate an improving economic momentum. Our nowcasts imply that the GDP of the U.S. will rise by 0.8% (3.2 annualized) in the U.S., by 0.4% in the Eurozone and there would be not growth in Finland in the third quarter. This reflects the improving momentum of the global economy driven by the gargantuan fiscal stimulus of the Biden administration and business cycle dynamics. The latter refers to the inherent cyclicality of economic activity, observed since the Roman times.1 Simplified, economies were heading down for so long that a (natural) bounce needed to occur. However, improved nowcasts mask an increasing underlying weakness, which we detail below.

Our forecasts for 2025 have also improved. This is also a feature of our model, where improved momentum carries forward. Yet, because the uncertainty concerning the 2025 forecasts is so massive, we will not speculate on them any further this time around.

Forecasts on the stimulus of China

Keep reading with a 7-day free trial

Subscribe to GnS Economics Newsletter to keep reading this post and get 7 days of free access to the full post archives.