The Coming Economic Collapse

The Coming Economic Collapse

Part I: Why are we here (on the verge)? (Free)

From Tuomas Malinen’s Forecasting Newsletter.

On Monday, I inquired on my followers, what topic should I cover next. 44% of the vote went to the option of analyzing the approaching economic collapse. This was a good result, imho, because it was a topic I have not visited for a while here, even though it has lingered in my mind. I think now is also a good time to re-visit the topic, because global recession is closing, which will bring a whole host of economic issues into the surface.

Economic collapse is also something we at GnS Economics have been warning since March 2017. In December 2017, we assessed that its first signs would appear in 2019, and they did. The near-collapse of credit markets in early January 2019, leading to the ‘pivot’ by the Federal Reserve, followed by a near-collapse of the U.S. repo-market in mid-September leading to the “Not-QE” by the Fed, signaled that the financial system was unable to stand without continuous central bank support. Essentially, without these ‘bailouts’ the crisis would have, most likely, commenced in 2019.

After a series of further bailouts, we now face a similar, but a much more daunting dilemma. The global economy is edging towards a recession with bloated public and private balance sheets. Governments, corporations and many households are more indebted than ever. This calls for a massive global bailout by central banks, if (when) the crisis hits, which would bear dire consequences.

This series consists on four parts. In this first one, I will outline the reasons why we are approaching an economic crisis of epic portions. In the second, I will explain how I see the collapse progressing, and the third provides a bit more detailed explanation on a cataclysmic economic event known as systemic meltdown. The last one presents estimates on the timeline of the collapse.

The first of these is free for all, while the rest will be (mostly) paywalled. We have a Summer campaign ongoing offering annual subscription with 15% off, which ends today.

Let’s dive in.

When central banks mess up

I think that we at GnS Economics summarized the main reason behind the coming collapse rather nicely in the June 2013 issue of our Q-Review. We noted that:

It is possible that the banking sector and the world economy were be saved by using too strong methods in 2008. As a consequence of this, it is also possible that the world economy is more like a zombie economy, where unprofitable banks and companies are kept alive with easy money and rescue packages from the governments.

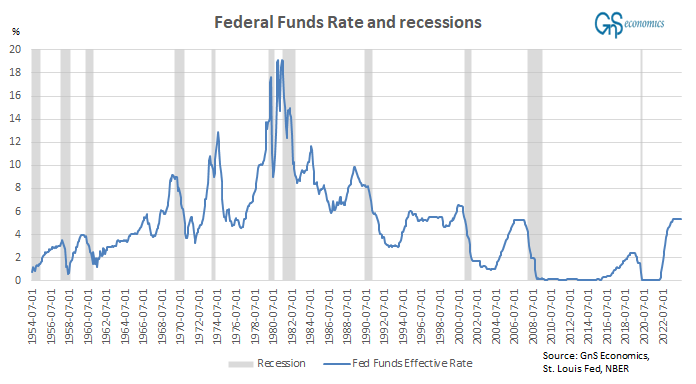

The interest rate policies of the Federal Reserve showcase this. Interest rates in the U.S. were kept near-zero from December 2008 till the end of 2015. Never before had interest rates been so close to zero, since the Great Depression.

The drastic interest rate policies enacted by the Fed were followed by several other central banks. The Bank of Japan (BoJ) had dropped interest rates to zero already in early 1999, and they were lifted to 0.5% in 2007 only to be dropped back to zero in the wake of the Great Financial Crisis (GFC) in 2009. Moreover, the ECB pushed rates to negative on 11 June 2014, with the BoJ following on 29 January 2016. The world entered into an era of financial perversion.

Central banks control short-term interest rates by setting the rate banks receive on their deposits, that is, on the reserves they hold at the central bank. The central bank sets the interest on the reserves and controls it by buying and selling securities in the markets, if necessary. Banks make majority of their profits from the interest rate differential between lending and borrowing (deposit taking). Specifically, the difference between lending and deposit rates usually determine the profitability of a bank. However, with very low interest rates, this difference becomes non-existent, and with negative rates, it inverts completely.1 When the profit margins of banks are squeezed, they start to cut back on lending, which further damages the profitability of banks. Moreover, because low and negative interest rate policies hurt the profitability of banks, they tend to target non-profitable firms, or zombie corporations (see below), in their lending practices to avert any further losses.

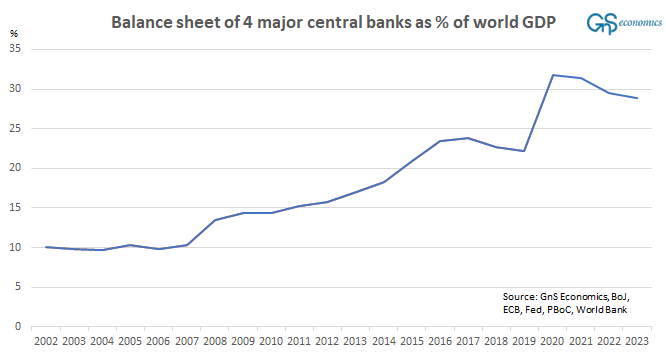

Another perverse innovation of central banks was to start to buy government bonds from the secondary markets. Probably to make such measures sound like a part of the arsenal of monetary policy, they were called as programs of quantitative easing, or QE. The Fed, who started the global cycle of QE-programs in October 2008,2 linked the QE tightly on the ability of a central bank to keep lowering long-term interest rates beyond 'zero lower bound', where short-term rates are near-zero losing their effectiveness to resuscitate the economy (or at least that’s how the current mainstream macroeconomic theory goes). Yet, QE-programs could have also been called a "partial socialization of the bond markets" to which they effectively evolved into.

Due to QE programs, the amount of money in circulation expanded massively, especially during the Corona bailout of spring 2020. They created cataclysmic distortions in the financial markets (see, e.g., this and this), and eventually led to emergence of rapid inflation. In a word, the asset-purchase programs of central bank have been an utter menace, and there’s more.

Zombies rule the earth

Zombies were introduced to the economic jargon by Ricardo Caballero, Takeo Hoshi and Anil Kashyap (2008) when they described the unproductive and indebted yet still operating firms in Japan as "zombie companies". They found that, after the financial crash of early 1990s, large Japanese banks kept money flowing to otherwise insolvent borrowers, aka zombies. The reason for this was that these large banks were itself in dire straits.

As I explained few weeks ago, the Japanese government encouraged banks to engage in false accounting to keep them operating in the financial crisis. The BoJ helped on this, by bailing out large financial institutions and by keeping interest rates low. These actions established a ‘zombified’ banking sector, where weak banks kept extending loans to their insolvent business customers to keep them from failing. As I also explained earlier, the policies enacted during and after the financial crisis led to the over-indebtedness of the Japanese government and thus to the ongoing currency crisis.

Zombie companies are a massive burden for the economy. They restrict the entry of new, more productive companies, diminish job creation in the economy and lock capital to unproductive use. When capital is locked to unproductive firms, this stall the productivity growth of the whole economy. Zombie companies seek to survive, not to thrive. They hoard money and debt, but do not invest. Workers may keep their jobs, but also they are locked in unprofitable production.

Taking the example of Japan into consideration, central bankers of the 2010s should have known to where their 'unconventional measures', i.e., zero and negative interest rates and QE programs would lead to, if they would be kept running for too long. Similarly, politicians should have known that countries should not allow insolvent banks to linger. Yet, this is exactly what they did.

The monetary and fiscal policy measures used to uphold the world economy after 2008 crisis were unprecedented. Never before had authorities in western capitalist countries taken such a large role in the economy in modern history. They should have known that all those exceptional measures would risk creating even bigger bubble and a fragile (zombified) global economy leading to an even bigger collapse down the line. Things went from bad to worse during the Corona bailout of the financial markets and the economy in the spring of 2020.

For example, in the case of the Fed, never before has a central bank tried singlehandedly to rescue both the financial system and a large proportion of U.S. corporations. However, this is exactly what the Fed did in March-June 2020. When the “corona-bailout” was complete, the FEd backstopped U.S. Treasury markets, intervened in corporate commercial-paper and municipal bond markets and short-term money-markets. It effectively became the financial markets, ending free capital markets in the U.S.

The collapse of growth in productivity

Long-term economic growth is driven by technical innovations, like the spinning-jenny and the modern industrial robots, which improve the productivity, that is, the efficiency of production. In essence, they increase the productivity of a human worker, which increases his wage and makes products cheaper. A process called creative destruction enables the flow of technological innovations into the production. The idea of creative destruction has been in the heart of market economies, practically, forever, but it was formalized by Joseph Schumpeter in Capitalism, Socialism and Democracy published in 1942.

In simplified terms, creative destruction is a process, where more efficient (more productive) methods replace the old and inefficient means of production. This naturally occurs both within firms, who replace unprofitable means of production with more profitable ones, but also within the overall economy. In the level of the economy, creative destruction presents itself as old, unprofitable firms failing and new more profitable firms taking their place. New, more profitable firms will foster productivity growth by enabling technological innovations to flow into production. This increases capital income, wages and our living standards. Another way to describe creative destruction is to note that both gains, i.e. successes and profits, as well as failures and bankruptcies of businesses drive economic progress and development.

The gains obtained from profitable production of goods and services accumulate income and capital, while failures uncover sustainable businesses. Capital seeks into these sustainable businesses and the cycle repeats. Governments can support this process by setting laws, providing infrastructure, governing human and property rights and guaranteeing income through social security, but it is the private sector, households, investors, corporations, entrepreneurs and the capital markets that drive the process of creative destruction. As the recurrent failures of socialist market economy experiments have shown, this risk-and-reward relationship is essential for the creative destruction and thus the economy to provide long-term gains in living standards and social stability.

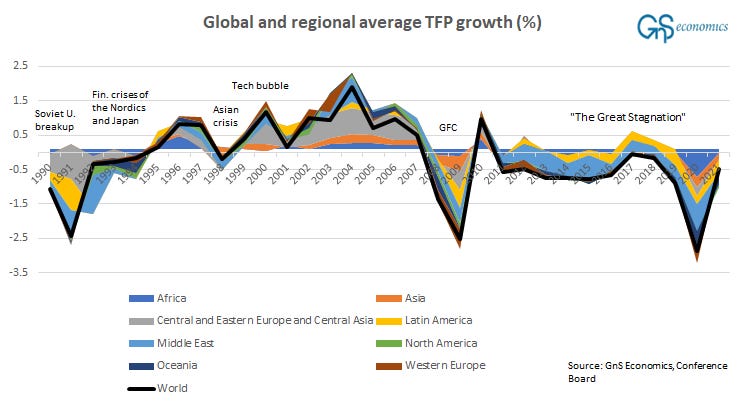

This continuous process of creation-destruction-creation is behind the spectacular rise in our living standards since the 18th century. However, political leaders and central bankers have removed or at least seriously distorted risk-and-reward relationships with their bailouts and monetary easing all around the globe since 2008. Market-wide losses and risks have been effectively socialized, but rewards, or profits, have remained (mostly) private. This "socialization" of the economy halted or at least seriously slowed the process of creative destruction, stagnating the growth of productivity, which is visible in the growth of Total Factor Productivity, or TFP.

The end is nigh

The fact is that since early 2009, we have lived in an artificially sustained economy. Monetary stimulus by central banks and the debt stimulus of China have kept the world economy growing, but in an utterly unsustainable way. Economies need to grow 'organically', that is, through growing productivity feeding into capital and wage income. Financial markets support this growth by creating financial innovations that, e.g., enable using future income now (debt) and hedging against business risks. This is how capitalist market economies were supposed to work. Central banks and Chinese authorities corrupted this after the financial crash of 2007-2008 and again, even more forcefully in 2020. The price for their errors will be steep.

When the growth of productivity stagnates, the economy turns fragile and dependent on debt to grow. More precisely, debt needs to grow ever faster to sustain the growth of the economy, because productivity is not growing. This implies that the income of economies, measured as the gross domestic product (GDP), is not growing, just debt.

Eventually a point of 'debt saturation', that is, a point where households and/or corporations cannot or will not be able to grow their debt pile anymore, is reached. This point tends to occur, when debt service costs exceed income growth with some sufficient margin. Usually this happens, when the economy starts to cool hurting income streams. Considering the massively bloated public and private balance sheets, how close are we to this point?

The second instalment dealing with the process of the collapse will be published next week.

Disclaimer:

The information contained herein is current as at the date of this entry. The information presented here is considered reliable, but its accuracy is not guaranteed. Changes may occur in the circumstances after the date of this entry and the information contained in this post may not hold true in the future.

No information contained in this entry should be construed as an investment advice nor advice on the safety of banks. GnS Economics nor any of the authors cannot be held responsible for errors or omissions in the data presented. Readers should always consult their own personal financial or investment before making any investment decision or decision on banks they hold their money in. Readers using this post do so solely at their own risk.

Readers must make an independent assessment of the risks involved and of the legal, tax, business, financial or other consequences of their actions. GnS Economics nor any of the authors cannot be held i) responsible for any decision taken, act or omission; or ii) liable for damages caused by such measures.

When a central bank drops rates to negative, banks need to pay interest on their central bank reserves. But, they are usually not relieved of the obligation to pay interest on customer deposits, who tend to be reluctant to pay interest on money they place at a bank. If banks are forced to pay interest on loans and receive interest on deposits, their whole earnings logic goes haywire.

The BoJ had run a similar program from March 2001 till March 2006. The funny thing is that the Bank stopped the program after its own research deemed the program as “non-effective”.